Page 1 of 1

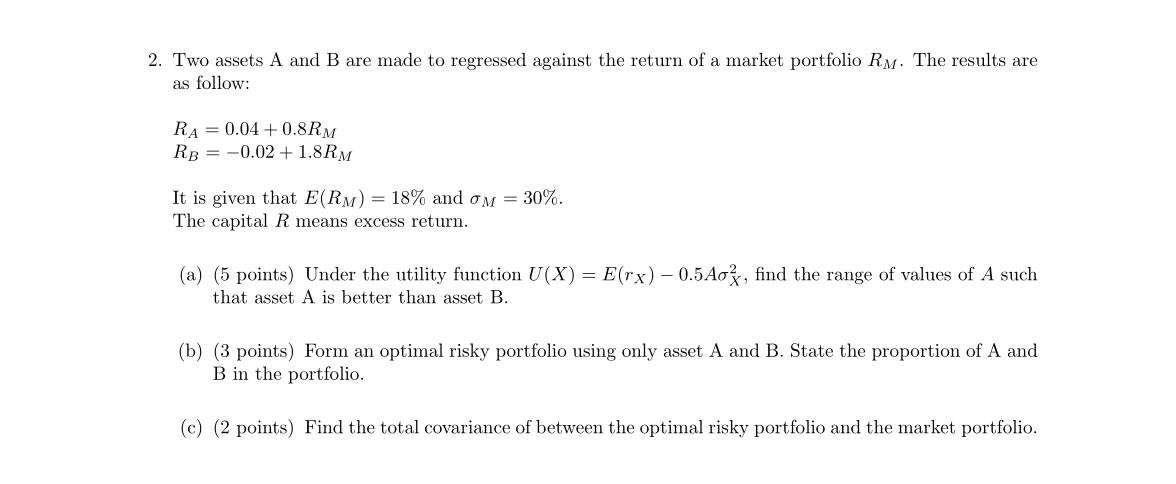

2. Two assets A and B are made to regressed against the return of a market portfolio Rm. The results are as follow: RA =

Posted: Tue Nov 23, 2021 8:58 am

by answerhappygod

- 2 Two Assets A And B Are Made To Regressed Against The Return Of A Market Portfolio Rm The Results Are As Follow Ra 1 (48.27 KiB) Viewed 98 times

2. Two assets A and B are made to regressed against the return of a market portfolio Rm. The results are as follow: RA = 0.04+0.8RM RB = -0.02 +1.8RM It is given that E(RM) = 18% and om = 30%. The capital R means excess return. (a) (5 points) Under the utility function U(X) = E(rx) - 0.5Aož, find the range of values of A such that asset A is better than asset B. (b) (3 points) Form an optimal risky portfolio using only asset A and B. State the proportion of A and B in the portfolio. (c) (2 points) Find the total covariance of between the optimal risky portfolio and the market portfolio.