Page 1 of 1

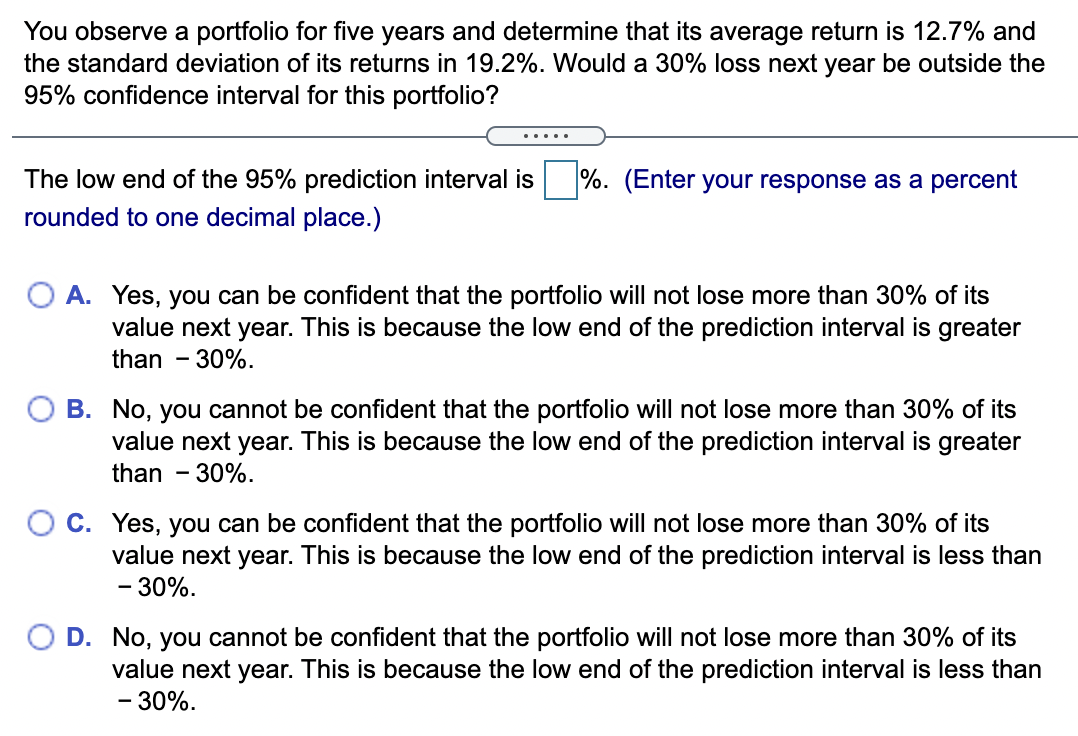

You observe a portfolio for five years and determine that its average return is 12.7% and the standard deviation of its

Posted: Tue Nov 23, 2021 8:51 am

by answerhappygod

- You Observe A Portfolio For Five Years And Determine That Its Average Return Is 12 7 And The Standard Deviation Of Its 1 (304.17 KiB) Viewed 141 times

You observe a portfolio for five years and determine that its average return is 12.7% and the standard deviation of its returns in 19.2%. Would a 30% loss next year be outside the a 95% confidence interval for this portfolio? %. (Enter your response as a percent The low end of the 95% prediction interval is rounded to one decimal place.) A. Yes, you can be confident that the portfolio will not lose more than 30% of its value next year. This is because the low end of the prediction interval is greater than -30%. B. No, you cannot be confident that the portfolio will not lose more than 30% of its value next year. This is because the low end of the prediction interval is greater than - 30%. C. Yes, you can be confident that the portfolio will not lose more than 30% of its value next year. This is because the low end of the prediction interval is less than -30%. D. No, you cannot be confident that the portfolio will not lose more than 30% of its value next year. This is because the low end of the prediction interval is less than - 30%.