Page 1 of 1

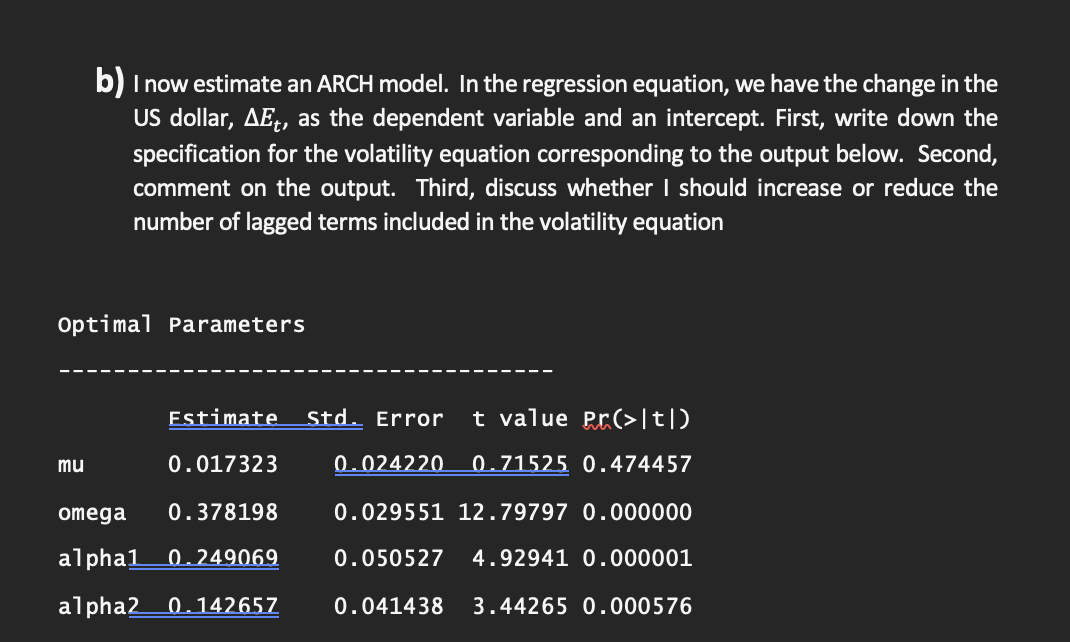

b) I now estimate an ARCH model. In the regression equation, we have the change in the US dollar, AEt, as the dependent

Posted: Thu May 19, 2022 10:49 am

by answerhappygod

- B I Now Estimate An Arch Model In The Regression Equation We Have The Change In The Us Dollar Aet As The Dependent 1 (67.3 KiB) Viewed 73 times

b) I now estimate an ARCH model. In the regression equation, we have the change in the US dollar, AEt, as the dependent variable and an intercept. First, write down the specification for the volatility equation corresponding to the output below. Second, comment on the output. Third, discuss whether I should increase or reduce the number of lagged terms included in the volatility equation Optimal Parameters Estimate Std. Error t value pr(>t) mu 0.017323 0.024220 0.71525 0.474457 omega 0.378198 0.029551 12.79797 0.000000 alpha1 0.249069 0.050527 4.92941 0.000001 alpha2 0.142657 0.041438 3.44265 0.000576