Page 1 of 1

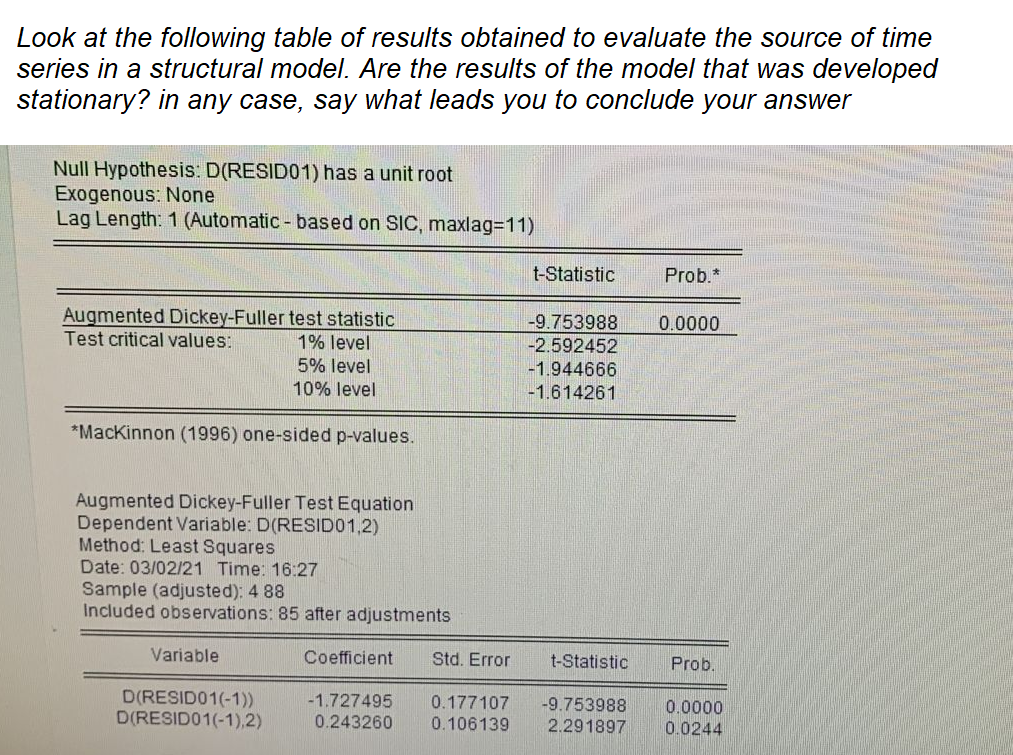

Look at the following table of results obtained to evaluate the source of time series in a structural model. Are the res

Posted: Thu May 19, 2022 9:28 am

by answerhappygod

- Look At The Following Table Of Results Obtained To Evaluate The Source Of Time Series In A Structural Model Are The Res 1 (1.15 MiB) Viewed 49 times

Look at the following table of results obtained to evaluate the source of time series in a structural model. Are the results of the model that was developed stationary? in any case, say what leads you to conclude your answer Null Hypothesis: D(RESID01) has a unit root Exogenous: None Lag Length: 1 (Automatic - based on SIC, maxlag=11) t-Statistic Prob.* 0.0000 Augmented Dickey-Fuller test statistic Test critical values: 1% level 5% level 10% level -9.753988 -2.592452 -1.944666 -1.614261 *Mackinnon (1996) one-sided p-values. Augmented Dickey-Fuller Test Equation Dependent Variable: D(RESID01,2) Method: Least Squares Date: 03/02/21 Time: 16:27 Sample (adjusted): 488 Included observations: 85 after adjustments Variable Coefficient Std. Error t-Statistic Prob D(RESIDO1(-1)) D(RESIDO1(-1),2) -1.727495 0.243260 0.177107 0.106139 -9.753988 2.291897 0.0000 0.0244