Page 1 of 1

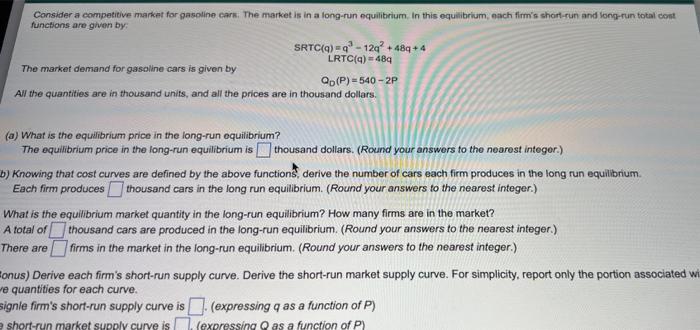

are by Consider a competitive market for gasoline cars. The market is in a long-run equilibrium In this equilibrium, eac

Posted: Thu May 19, 2022 9:02 am

by answerhappygod

- Are By Consider A Competitive Market For Gasoline Cars The Market Is In A Long Run Equilibrium In This Equilibrium Eac 1 (46.74 KiB) Viewed 136 times

are by Consider a competitive market for gasoline cars. The market is in a long-run equilibrium In this equilibrium, each firm's shon-run and long-run total cont SRTC(q) =q2 - 120? +48q+4 LRTC(q) =484 The market demand for gasoline cars is given by Q.(P)=540-2P All the quantities are in thousand units, and all the prices are in thousand dollars. (a) What is the equilibrium price in the long-run equilibrium? The equilibrium price in the long-run equilibrium is thousand dollars. (Round your answers to the nearest Integer.) b) Knowing that cost curves are defined by the above functions, derive the number of cars each firm produces in the long run equilibrium Each firm produces thousand cars in the long run equilibrium (Round your answers to the nearest integer.) What is the equilibrium market quantity in the long-run equilibrium? How many firms are in the market? A total of thousand cars are produced in the long-run equilibrium. (Round your answers to the nearest integer.) firms in the market in the long-run equilibrium. (Round your answers to the nearest integer.) tonus) Derive each firm's short-run supply curve. Derive the short-run market supply curve. For simplicity, report only the portion associated wi e quantities for each curve. signle firm's short-run supply curve is (expressing q as a function of P) short-run market supply curve is expressing as a function of PM There are