Page 1 of 1

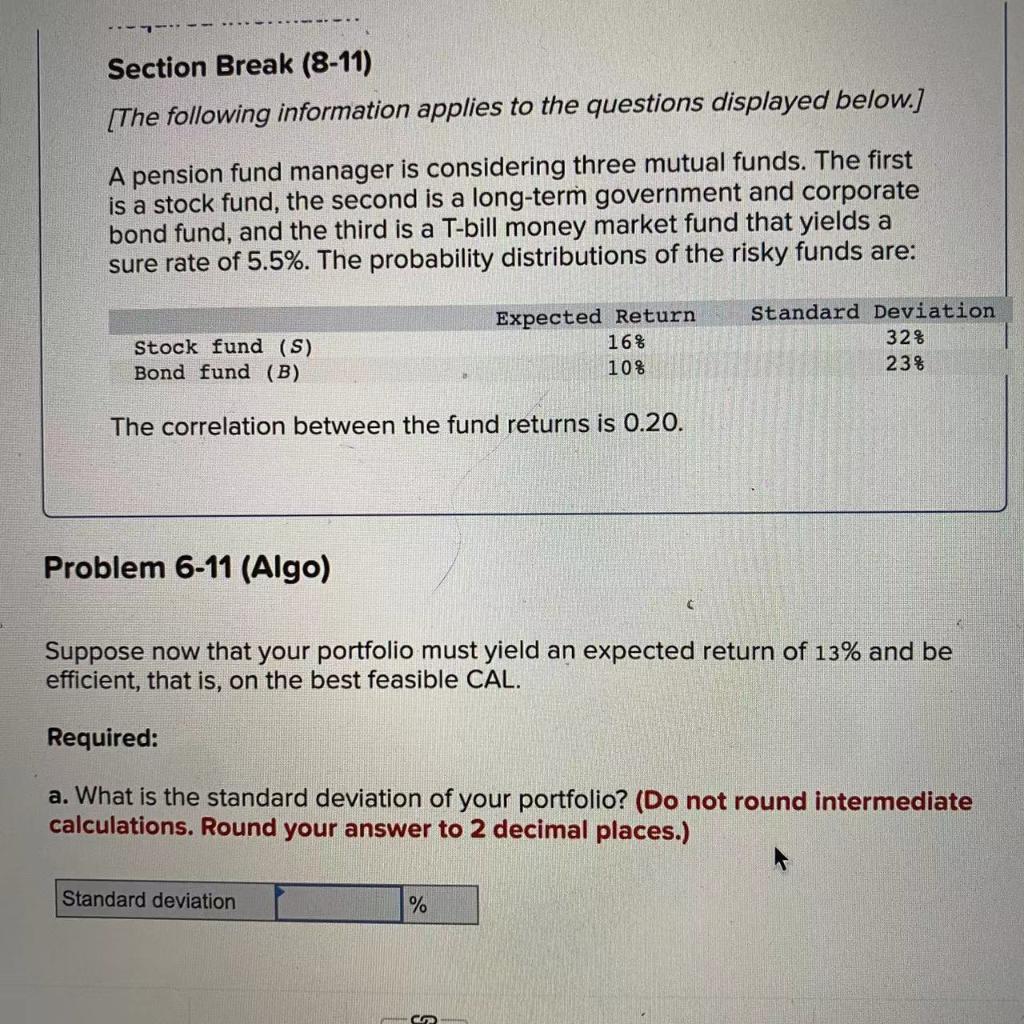

Section Break (8-11) [The following information applies to the questions displayed below.] A pension fund manager is con

Posted: Wed May 18, 2022 11:58 pm

by answerhappygod

- Section Break 8 11 The Following Information Applies To The Questions Displayed Below A Pension Fund Manager Is Con 1 (206.94 KiB) Viewed 56 times

Section Break (8-11) [The following information applies to the questions displayed below.] A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Stock fund (S) Bond fund (B) Expected Return 16% 10% Standard Deviation 32% 23% The correlation between the fund returns is 0.20. Problem 6-11 (Algo) Suppose now that your portfolio must yield an expected return of 13% and be efficient, that is, on the best feasible CAL. Required: a. What is the standard deviation of your portfolio? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Standard deviation %