Page 1 of 1

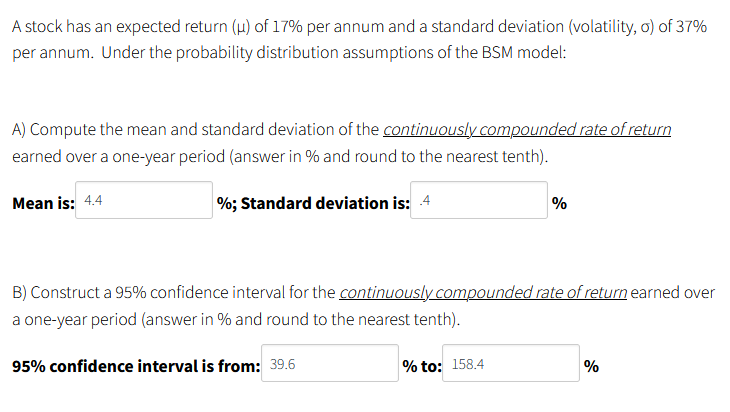

A stock has an expected return () of 17% per annum and a standard deviation (volatility, o) of 37% per annum. Under the

Posted: Wed May 18, 2022 11:40 pm

by answerhappygod

- A Stock Has An Expected Return Of 17 Per Annum And A Standard Deviation Volatility O Of 37 Per Annum Under The 1 (44.83 KiB) Viewed 47 times

A stock has an expected return () of 17% per annum and a standard deviation (volatility, o) of 37% per annum. Under the probability distribution assumptions of the BSM model: A) Compute the mean and standard deviation of the continuously compounded rate of return earned over a one-year period (answer in % and round to the nearest tenth). Mean is: 4.4 %; Standard deviation is: .4 % B) Construct a 95% confidence interval for the continuously compounded rate of return earned over a one-year period (answer in % and round to the nearest tenth). 95% confidence interval is from: 39.6 % to: 158.4 %