Page 1 of 1

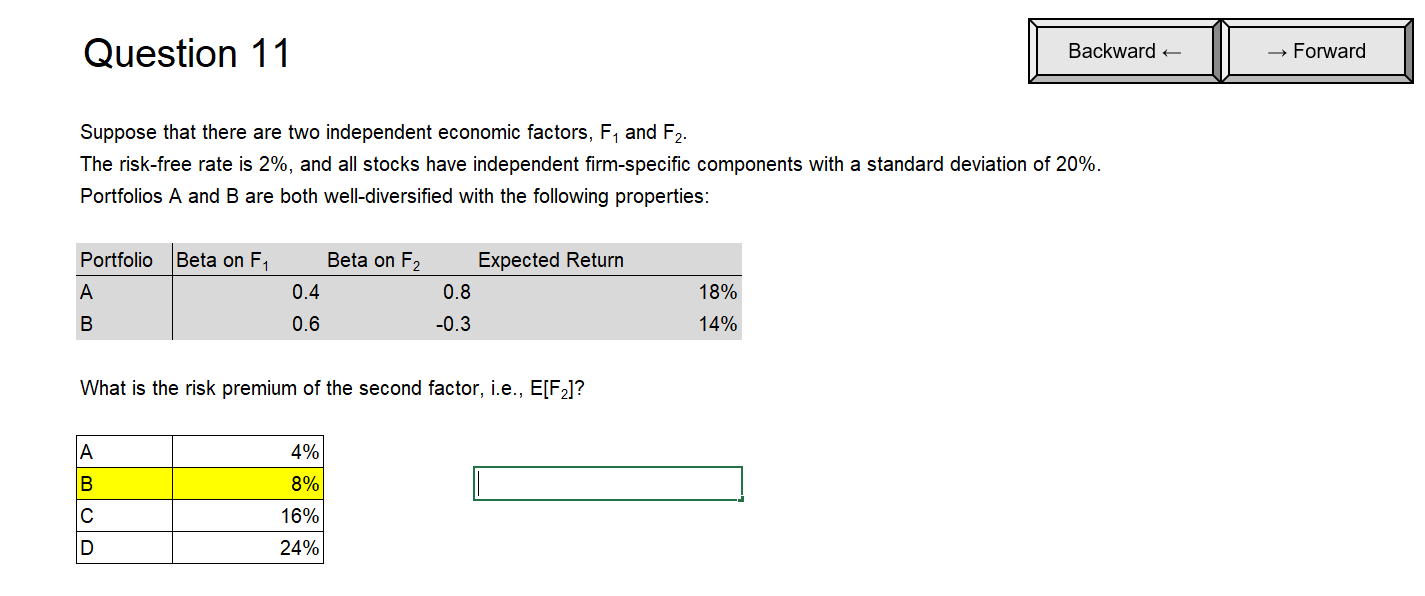

Question 11 Backward Forward Suppose that there are two independent economic factors, F, and F2. The risk-free rate is 2

Posted: Wed May 18, 2022 10:41 pm

by answerhappygod

- Question 11 Backward Forward Suppose That There Are Two Independent Economic Factors F And F2 The Risk Free Rate Is 2 1 (31.44 KiB) Viewed 78 times

Question 11 Backward Forward Suppose that there are two independent economic factors, F, and F2. The risk-free rate is 2%, and all stocks have independent firm-specific components with a standard deviation of 20%. Portfolios A and B are both well-diversified with the following properties: Portfolio Beta on F1 Beta on F2 Expected Return 0.8 A 0.4 18% B 0.6 -0.3 14% What is the risk premium of the second factor, i.e., E[F]? A 4% B 8% IM00 16% 24%