Page 1 of 1

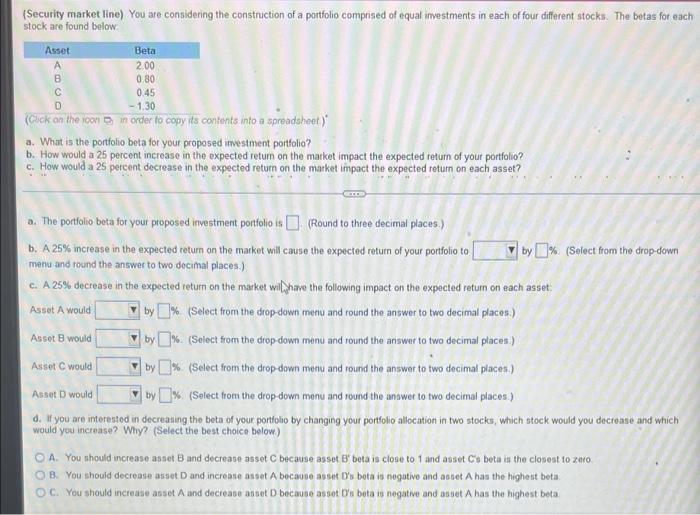

(Security market line) You are considering the construction of a portfolio comprised of equal investments in each of fou

Posted: Wed May 18, 2022 10:18 pm

by answerhappygod

- Security Market Line You Are Considering The Construction Of A Portfolio Comprised Of Equal Investments In Each Of Fou 1 (60.25 KiB) Viewed 64 times

(Security market line) You are considering the construction of a portfolio comprised of equal investments in each of four different stocks. The betas for each stock are found below Asset COOO D Beta 2.00 0 80 0.45 -1.30 (Click on the icon in order to copy its contents into a spreadsheet) a. What is the portfolio beta for your proposed investment portfolio? b. How would a 25 percent increase in the expected return on the market impact the expected return of your portfolio? c. How would a 25 percent decrease in the expected return on the market impact the expected return on each asset? 2. The portfolio bota for your proposed investment portfolio is (Round to three decimal places.) b. A 25% increase in the expected return on the market will cause the expected return of your portfolio to by % (Select from the drop-down menu and round the answer to two decimal places.) c. A 25% decrease in the expected return on the market will have the following impact on the expected return on each asset Asset A would V by % (Select from the drop-down menu and round the answer to two decimal places.) Asset B would V by % (Select from the drop down menu and round the answer to two decimal places) Asset C would by % (Select from the drop down menu and round the answer to two decimal places) Asset would by % (Select from the drop down menu and round the answer to two decimal places.) d. If you are interested in decreasing the beta of your portfolio by changing your portfolio allocation in two stocks, which stock would you decrease and which would you increase? Why? (Select the best choice below) OA. You should increase asset B and decrease asset C because asset Bbeta is close to 1 and asset C's beta is the closest to zero OB. You should decrease asset and increase onset A because asset D's beta is negative and asset A has the highest beta OC. You should increase asset A and decrease asset D because as set D's beta is negative and asset A has the highest beta