Page 1 of 1

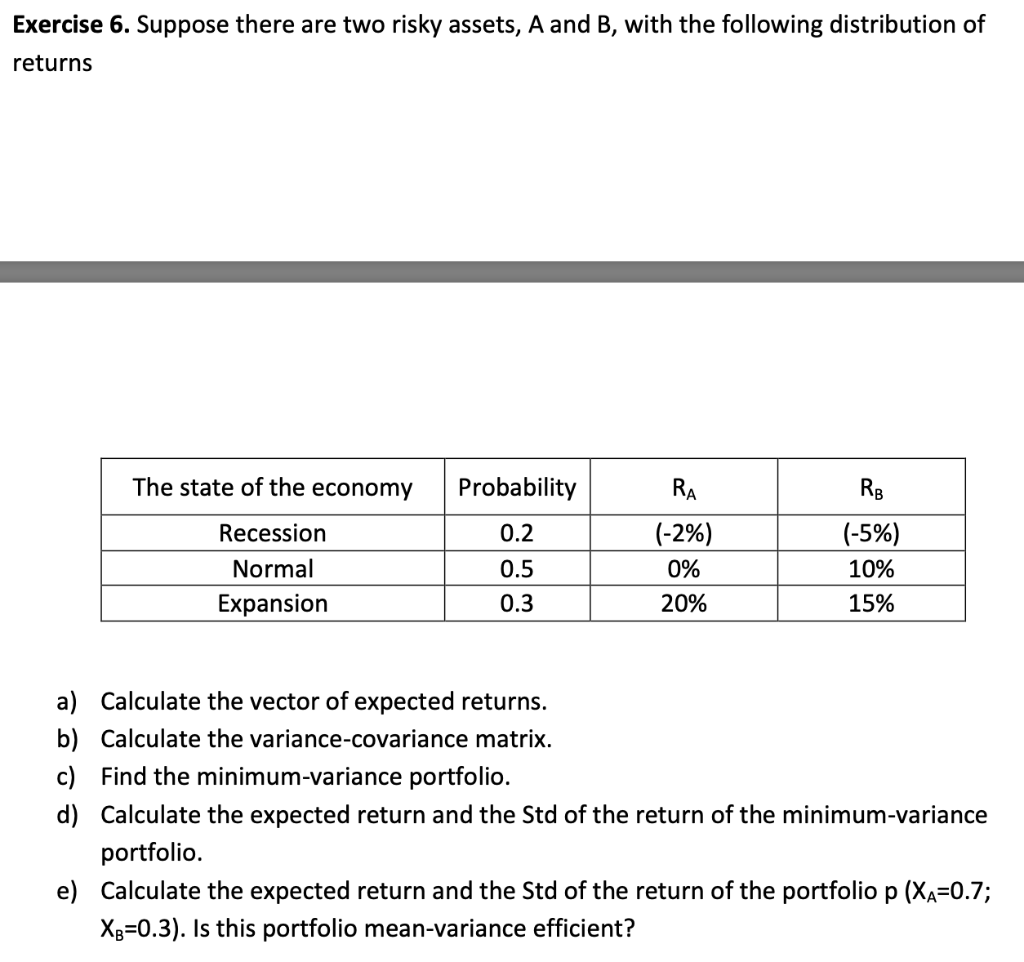

Exercise 6. Suppose there are two risky assets, A and B, with the following distribution of returns The state of the eco

Posted: Wed May 18, 2022 10:14 pm

by answerhappygod

- Exercise 6 Suppose There Are Two Risky Assets A And B With The Following Distribution Of Returns The State Of The Eco 1 (114.98 KiB) Viewed 51 times

Exercise 6. Suppose there are two risky assets, A and B, with the following distribution of returns The state of the economy Probability RB Recession Normal Expansion 0.2 0.5 0.3 RA (-2%) 0% 20% (-5%) 10% 15% a) Calculate the vector of expected returns. b) Calculate the variance-covariance matrix. c) Find the minimum-variance portfolio. d) Calculate the expected return and the Std of the return of the minimum-variance portfolio. e) Calculate the expected return and the Std of the return of the portfolio p (Xa=0.7; Xg=0.3). Is this portfolio mean-variance efficient?