Page 1 of 1

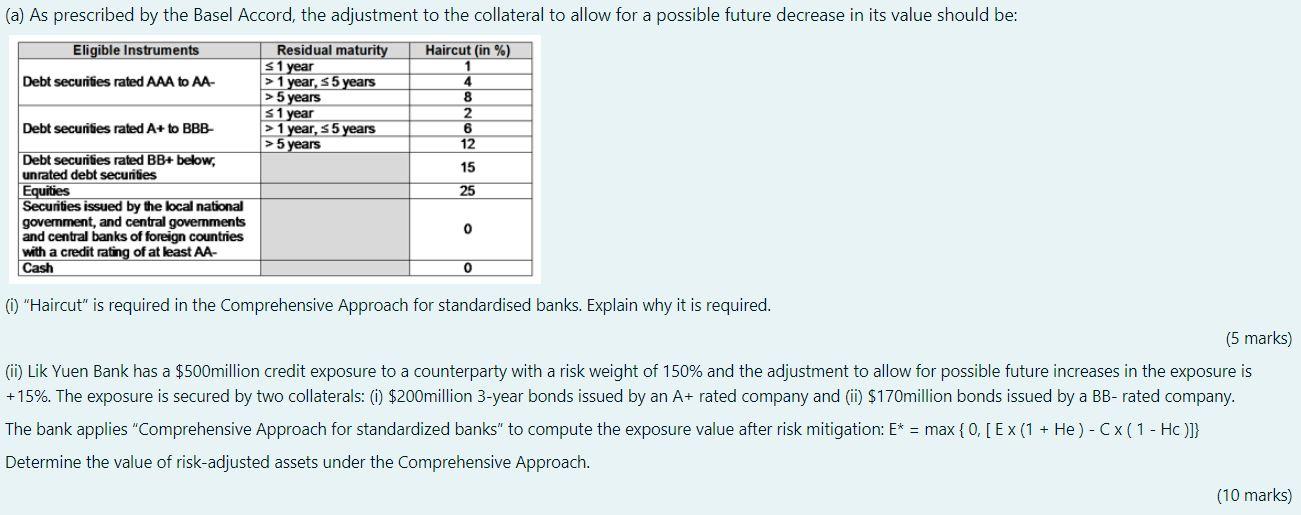

(a) As prescribed by the Basel Accord, the adjustment to the collateral to allow for a possible future decrease in its v

Posted: Wed May 18, 2022 9:36 pm

by answerhappygod

- A As Prescribed By The Basel Accord The Adjustment To The Collateral To Allow For A Possible Future Decrease In Its V 1 (92.98 KiB) Viewed 43 times

(a) As prescribed by the Basel Accord, the adjustment to the collateral to allow for a possible future decrease in its value should be: Eligible Instruments Haircut (in %) Debt securities rated AAA to AA- Residual maturity 5 1 year > 1 year, 55 years >5 years 5 1 year > 1 year, s 5 years >5 years 4 8 2 6 12 Debt securities rated A+ to BBB- 15 25 Debt securities rated BB+ below, unrated debt securities Equities Securities issued by the local national government, and central governments and central banks of foreign countries with a credit rating of at least AA- Cash o 0 ("Haircut" is required in the Comprehensive Approach for standardised banks. Explain why it is required. (5 marks) (ii) Lik Yuen Bank has a $500million credit exposure to a counterparty with a risk weight of 150% and the adjustment to allow for possible future increases in the exposure is +15%. The exposure is secured by two collaterals: (0) $200 million 3-year bonds issued by an A+ rated company and (ii) $170million bonds issued by a BB-rated company. The bank applies "Comprehensive Approach for standardized banks" to compute the exposure value after risk mitigation: E* = max {0, [ Ex (1 + He) - CX(1 - HC )]} Determine the value of risk-adjusted assets under the Comprehensive Approach. (10 marks)