Page 1 of 1

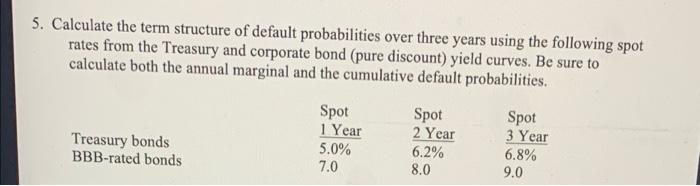

5. Calculate the term structure of default probabilities over three years using the following spot rates from the Treasu

Posted: Tue Nov 16, 2021 8:36 am

by answerhappygod

- 5 Calculate The Term Structure Of Default Probabilities Over Three Years Using The Following Spot Rates From The Treasu 1 (18.06 KiB) Viewed 124 times

5. Calculate the term structure of default probabilities over three years using the following spot rates from the Treasury and corporate bond (pure discount) yield curves. Be sure to calculate both the annual marginal and the cumulative default probabilities. Treasury bonds BBB-rated bonds Spot 1 Year 5.0% 7.0 Spot 2 Year 6.2% 8.0 Spot 3 Year 6.8% 9.0