Page 1 of 1

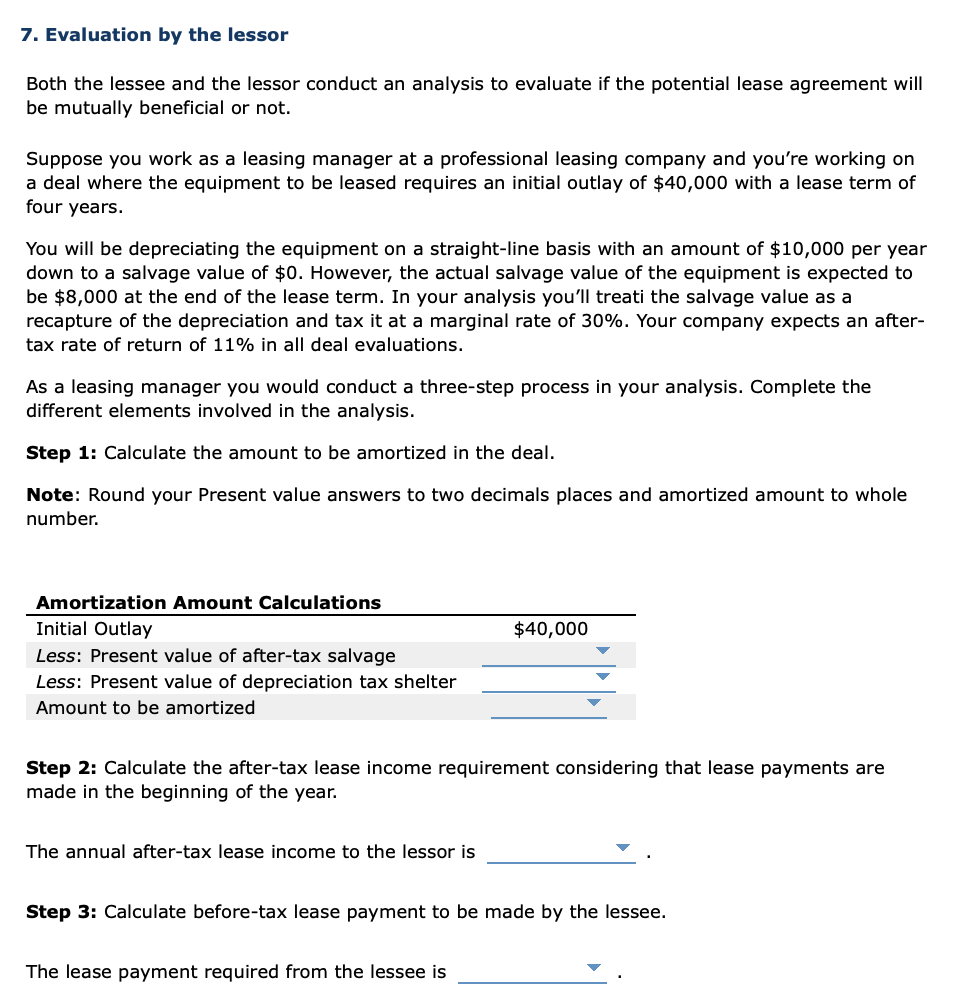

7. Evaluation by the lessor Both the lessee and the lessor conduct an analysis to evaluate if the potential lease agreem

Posted: Tue Nov 16, 2021 8:33 am

by answerhappygod

- 7 Evaluation By The Lessor Both The Lessee And The Lessor Conduct An Analysis To Evaluate If The Potential Lease Agreem 1 (124.78 KiB) Viewed 146 times

7. Evaluation by the lessor Both the lessee and the lessor conduct an analysis to evaluate if the potential lease agreement will be mutually beneficial or not. Suppose you work as a leasing manager at a professional leasing company and you're working on a deal where the equipment to be leased requires an initial outlay of $40,000 with a lease term of four years. You will be depreciating the equipment on a straight-line basis with an amount of $10,000 per year down to a salvage value of $0. However, the actual salvage value of the equipment is expected to be $8,000 at the end of the lease term. In your analysis you'll treati the salvage value as a recapture of the depreciation and tax it at a marginal rate of 30%. Your company expects an after- tax rate of return of 11% in all deal evaluations. As a leasing manager you would conduct a three-step process in your analysis. Complete the different elements involved in the analysis. Step 1: Calculate the amount to be amortized in the deal. Note: Round your Present value answers to two decimals places and amortized amount to whole number. $40,000 Amortization Amount Calculations Initial Outlay Less: Present value of after-tax salvage Less: Present value of depreciation tax shelter Amount to be amortized Step 2: Calculate the after-tax lease income requirement considering that lease payments are made in the beginning of the year. The annual after-tax lease income to the lessor is Step 3: Calculate before-tax lease payment to be made by the lessee. The lease payment required from the lessee is