Page 1 of 1

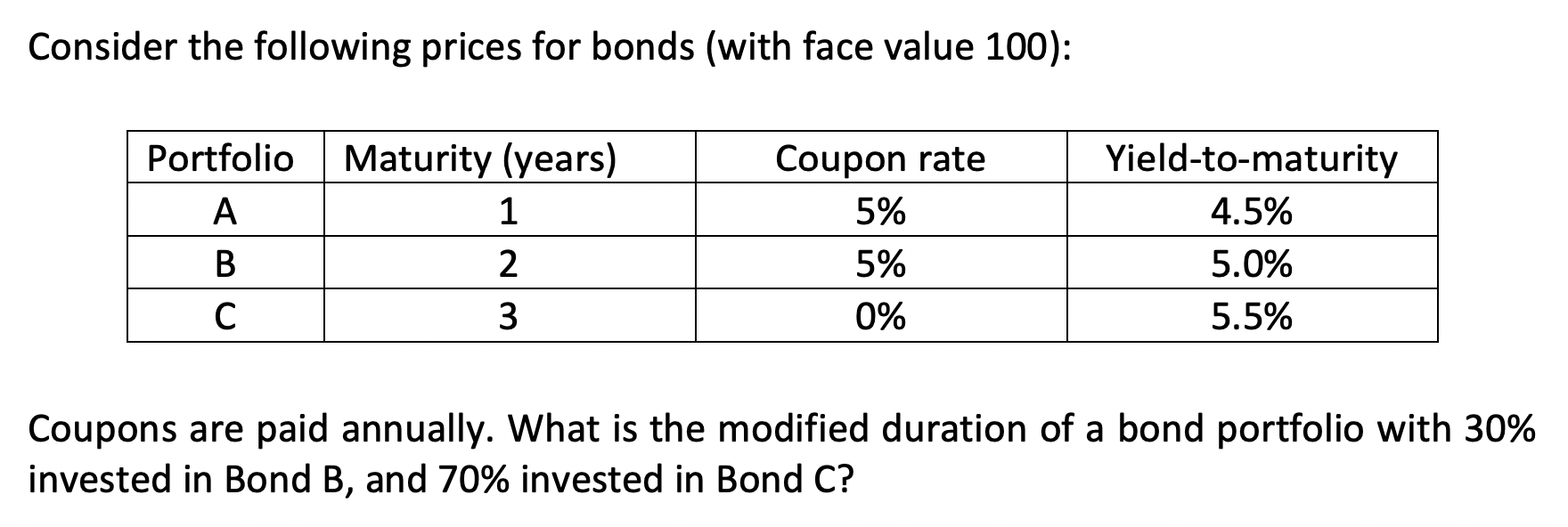

Consider the following prices for bonds (with face value 100): Portfolio Maturity (years) 1 A Coupon rate 5% 5% 0% Yield

Posted: Tue Nov 16, 2021 8:19 am

by answerhappygod

- Consider The Following Prices For Bonds With Face Value 100 Portfolio Maturity Years 1 A Coupon Rate 5 5 0 Yield 1 (215.86 KiB) Viewed 187 times

Consider the following prices for bonds (with face value 100): Portfolio Maturity (years) 1 A Coupon rate 5% 5% 0% Yield-to-maturity 4.5% 5.0% 5.5% 2 B С Nm 3 Coupons are paid annually. What is the modified duration of a bond portfolio with 30% a invested in Bond B, and 70% invested in Bond C?