Page 1 of 1

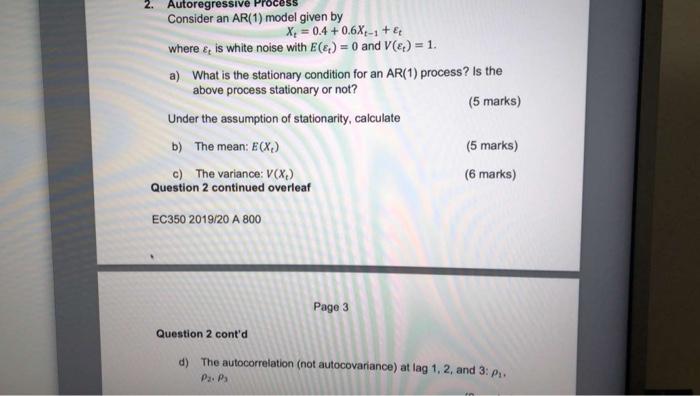

2. Autoregressive Consider an AR(1) model given by X = 0.4 +0.6X-1 + where & is white noise with E(€) = 0 and V(!) = 1.

Posted: Tue May 17, 2022 8:20 pm

by answerhappygod

- 2 Autoregressive Consider An Ar 1 Model Given By X 0 4 0 6x 1 Where Is White Noise With E 0 And V 1 1 (32.05 KiB) Viewed 33 times

2. Autoregressive Consider an AR(1) model given by X = 0.4 +0.6X-1 + where & is white noise with E(€) = 0 and V(!) = 1. a) What is the stationary condition for an AR(1) process? Is the above process stationary or not? (5 marks) Under the assumption of stationarity, calculate b) The mean: E(X) (5 marks) c) The variance: V(X) (6 marks) Question 2 continued overleaf EC350 2019/20 A 800 Page 3 Question 2 cont'd d) The autocorrelation (not autocovariance) at lag 1, 2 and 3: P. P2. Po