Page 1 of 1

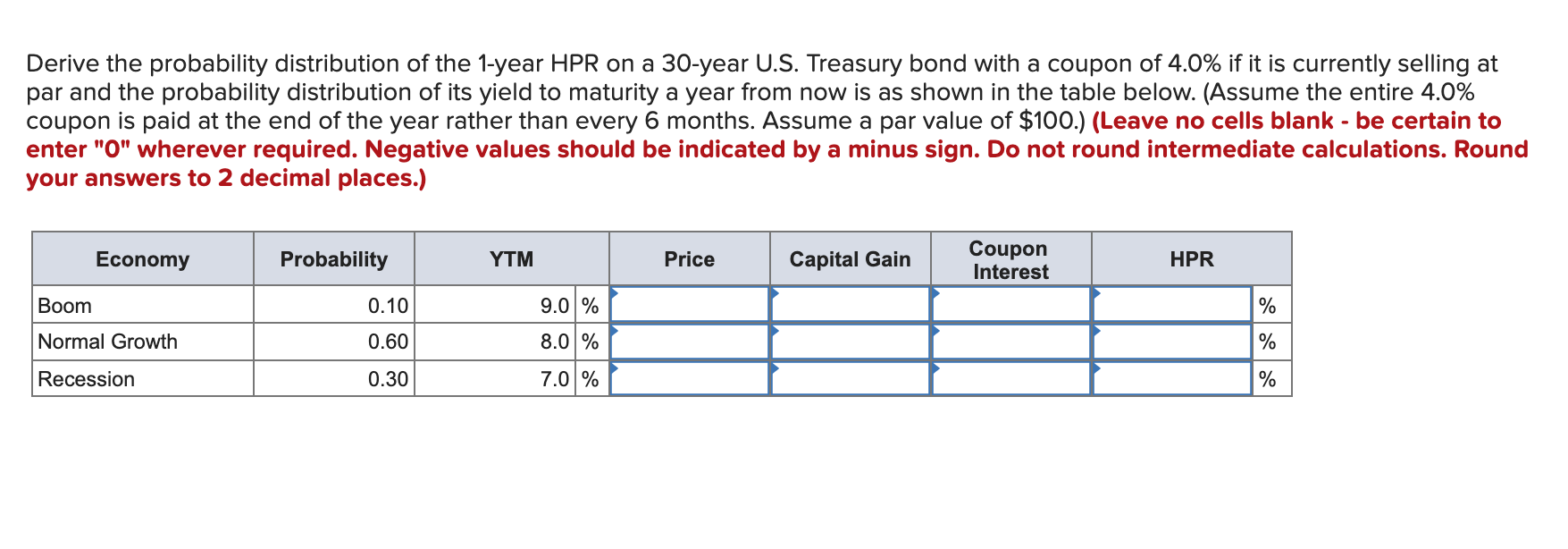

Derive the probability distribution of the 1-year HPR on a 30-year U.S. Treasury bond with a coupon of 4.0% if it is cur

Posted: Tue Nov 16, 2021 7:46 am

by answerhappygod

- Derive The Probability Distribution Of The 1 Year Hpr On A 30 Year U S Treasury Bond With A Coupon Of 4 0 If It Is Cur 1 (91.77 KiB) Viewed 93 times

Derive the probability distribution of the 1-year HPR on a 30-year U.S. Treasury bond with a coupon of 4.0% if it is currently selling at par and the probability distribution of its yield to maturity a year from now is as shown in the table below. (Assume the entire 4.0% coupon is paid at the end of the year rather than every 6 months. Assume a par value of $100.) (Leave no cells blank - be certain to enter "O" wherever required. Negative values should be indicated by a minus sign. Do not round intermediate calculations. Round your answers to 2 decimal places.) Economy Probability YTM Price Capital Gain Coupon Interest HPR Boom 0.10 9.0 % % Normal Growth 0.60 8.0 % % Recession 0.30 7.0 % %