Page 1 of 1

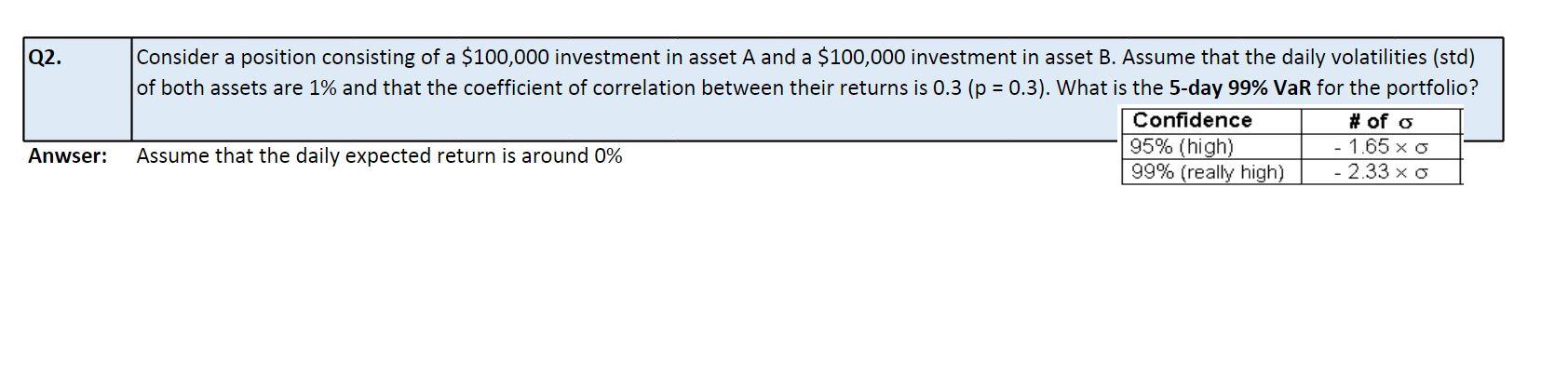

Q2. Consider a position consisting of a $100,000 investment in asset A and a $100,000 investment in asset B. Assume that

Posted: Tue Nov 16, 2021 7:38 am

by answerhappygod

- Q2 Consider A Position Consisting Of A 100 000 Investment In Asset A And A 100 000 Investment In Asset B Assume That 1 (65.87 KiB) Viewed 130 times

Q2. Consider a position consisting of a $100,000 investment in asset A and a $100,000 investment in asset B. Assume that the daily volatilities (std) of both assets are 1% and that the coefficient of correlation between their returns is 0.3 (p = 0.3). What is the 5-day 99% VaR for the portfolio? Confidence # of o 95% (high) - 165 x 3 Assume that the daily expected return is around 0% 99% (really high) 233 x 3 Anwser: