Page 1 of 1

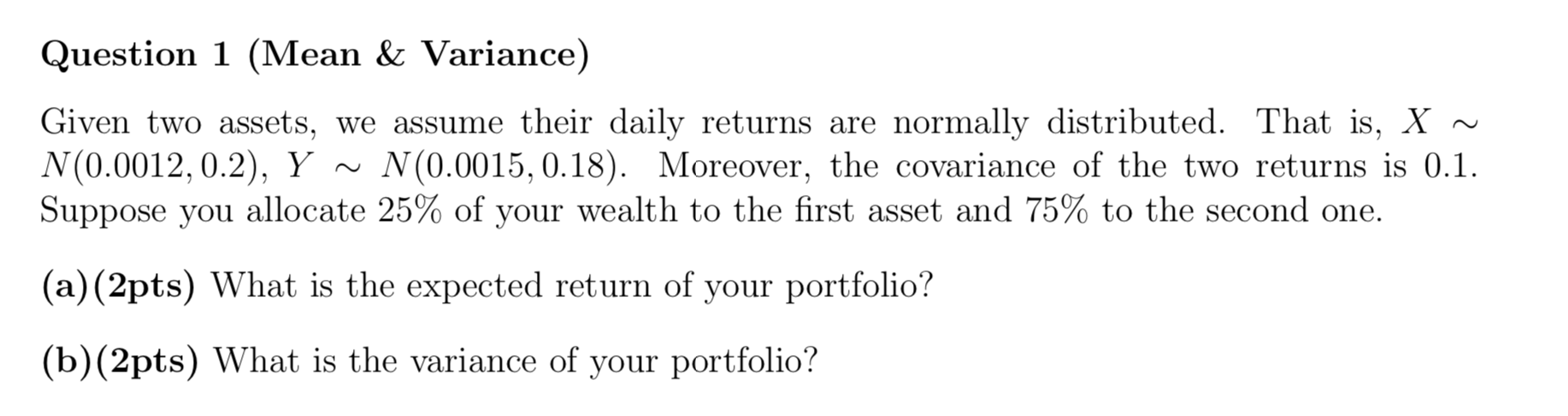

Question 1 (Mean & Variance) Given two assets, we assume their daily returns are normally distributed. That is, X- N(0.0

Posted: Sun Sep 05, 2021 5:00 pm

by answerhappygod

- Question 1 Mean Variance Given Two Assets We Assume Their Daily Returns Are Normally Distributed That Is X N 0 0 1 (96.87 KiB) Viewed 711 times

Question 1 (Mean & Variance) Given two assets, we assume their daily returns are normally distributed. That is, X- N(0.0012,0.2), Y ~ N(0.0015, 0.18). Moreover, the covariance of the two returns is 0.1. Suppose you allocate 25% of your wealth to the first asset and 75% to the second one. (a)(2pts) What is the expected return of your portfolio? (b)(2pts) What is the variance of your portfolio?