Page 1 of 1

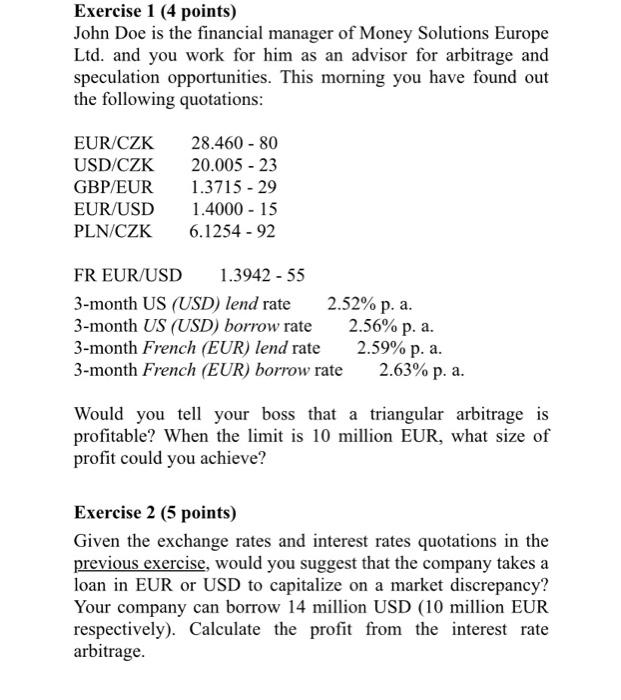

Exercise 1 (4 points) John Doe is the financial manager of Money Solutions Europe Ltd. and you work for him as an adviso

Posted: Mon Nov 15, 2021 5:03 pm

by answerhappygod

- Exercise 1 4 Points John Doe Is The Financial Manager Of Money Solutions Europe Ltd And You Work For Him As An Adviso 1 (64.66 KiB) Viewed 99 times

Exercise 1 (4 points) John Doe is the financial manager of Money Solutions Europe Ltd. and you work for him as an advisor for arbitrage and speculation opportunities. This morning you have found out the following quotations: EUR/CZK USD/CZK GBP/EUR EUR/USD PLN/CZK 28.460 - 80 20.005 - 23 1.3715-29 1.4000 - 15 6.1254 - 92 FR EUR/USD 1.3942 - 55 3-month US (USD) lend rate 2.52% p. a. 3-month US (USD) borrow rate 2.56% p. a. 3-month French (EUR) lend rate 2.59% p. a. 3-month French (EUR) borrow rate 2.63% p. a. Would you tell your boss that a triangular arbitrage is profitable? When the limit is 10 million EUR, what size of profit could you achieve? Exercise 2 (5 points) Given the exchange rates and interest rates quotations in the previous exercise, would you suggest that the company takes a loan in EUR or USD to capitalize on a market discrepancy? Your company can borrow 14 million USD (10 million EUR respectively). Calculate the profit from the interest rate arbitrage.