Page 1 of 1

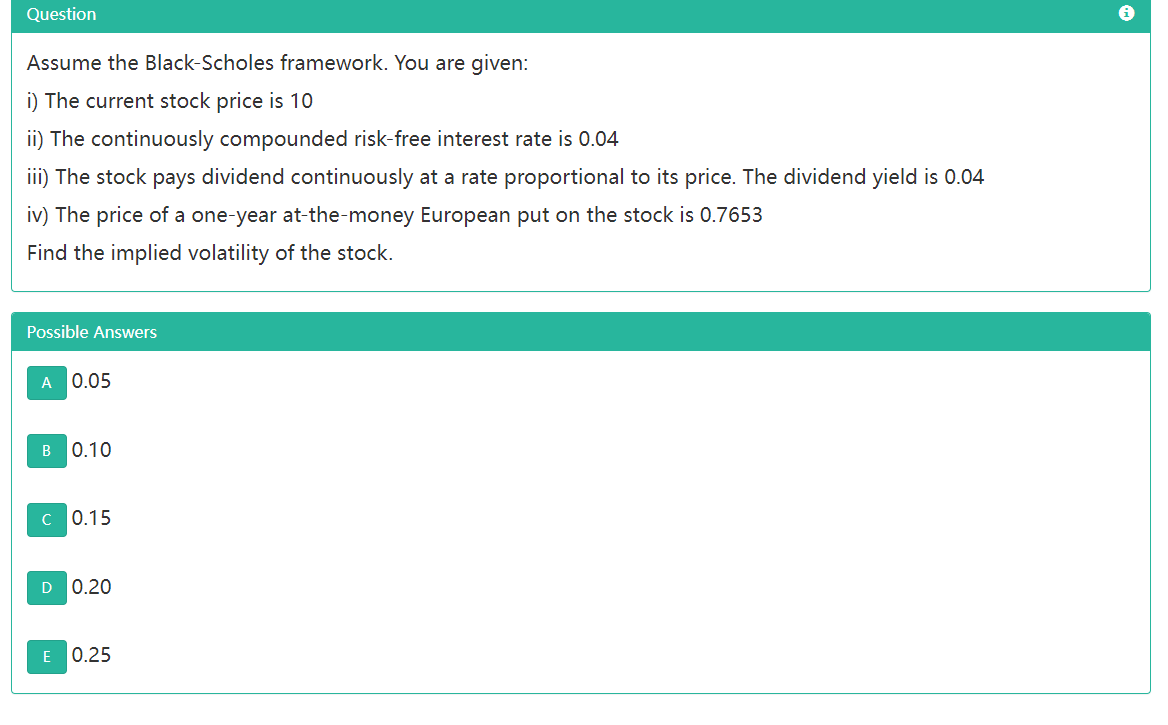

Question Assume the Black-Scholes framework. You are given: i) The current stock price is 10 ii) The continuously compou

Posted: Mon Nov 15, 2021 5:01 pm

by answerhappygod

- Question Assume The Black Scholes Framework You Are Given I The Current Stock Price Is 10 Ii The Continuously Compou 1 (28.44 KiB) Viewed 87 times

Question Assume the Black-Scholes framework. You are given: i) The current stock price is 10 ii) The continuously compounded risk-free interest rate is 0.04 iii) The stock pays dividend continuously at a rate proportional to its price. The dividend yield is 0.04 iv) The price of a one-year at-the-money European put on the stock is 0.7653 Find the implied volatility of the stock. Possible Answers A 0.05 B 0.10 C 0.15 D 0.20 E 0.25