Page 1 of 1

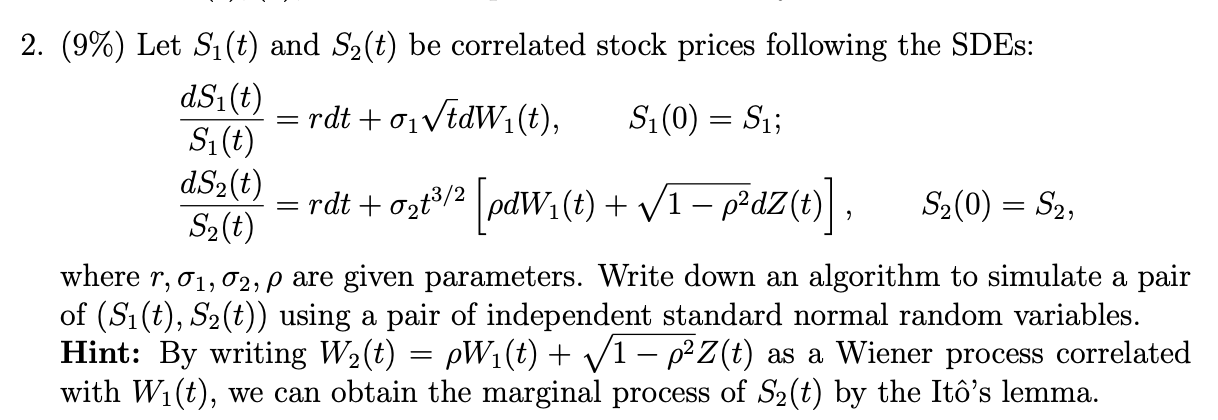

= = 2. (9%) Let Si(t) and S2(t) be correlated stock prices following the SDEs: dSi(t) = rdt +01VtdWi(t), Si(0) = Su; S(t

Posted: Thu May 12, 2022 12:49 pm

by answerhappygod

- 2 9 Let Si T And S2 T Be Correlated Stock Prices Following The Sdes Dsi T Rdt 01vtdwi T Si 0 Su S T 1 (84.11 KiB) Viewed 32 times

= = 2. (9%) Let Si(t) and S2(t) be correlated stock prices following the SDEs: dSi(t) = rdt +01VtdWi(t), Si(0) = Su; S(t) dS2(t) = rdt + o2t3/2 (pdW. (t) + V1 – p?dz(t)] S2(0) = S2, S2(t) where r, 01, 02, p are given parameters. Write down an algorithm to simulate a pair of (Si(t), S2(t)) using a pair of independent standard normal random variables. Hint: By writing W2(t) = pWi(t) + V1 - p2Z(t) as a Wiener process correlated with Wi(t), we can obtain the marginal process of S2(t) by the Itô’s lemma. 2 =