Page 1 of 1

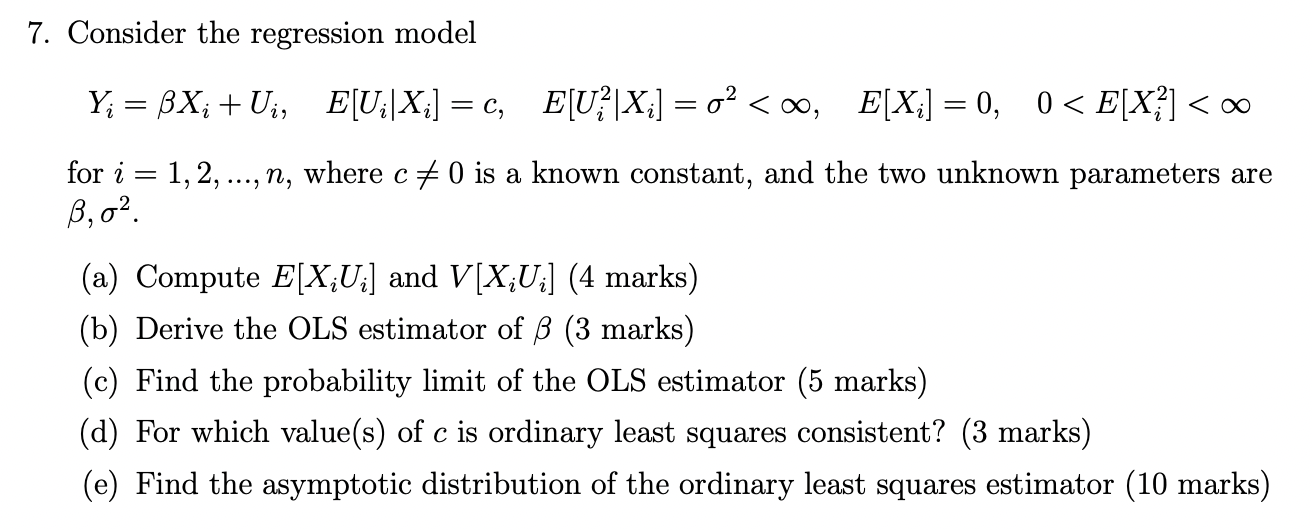

7. Consider the regression model Y; = BX; +Ui, E[U|X] = C, E[U?|Xj] = o? <, E[X]] = 0, 0 < E[X?] < 00 = a for i = 1, 2,

Posted: Wed May 11, 2022 8:30 pm

by answerhappygod

- 7 Consider The Regression Model Y Bx Ui E U X C E U Xj O E X 0 0 E X 00 A For I 1 2 1 (210.83 KiB) Viewed 27 times

7. Consider the regression model Y; = BX; +Ui, E[U|X] = C, E[U?|Xj] = o? <, E[X]] = 0, 0 < E[X?] < 00 = a for i = 1, 2, ..., n, where c# 0 is a known constant, and the two unknown parameters are B, o? (a) Compute E[X;U;] and V[X;U;] (4 marks) (b) Derive the OLS estimator of B (3 marks) (c) Find the probability limit of the OLS estimator (5 marks) (d) For which value(s) of c is ordinary least squares consistent? (3 marks) (e) Find the asymptotic distribution of the ordinary least squares estimator (10 marks)