Page 1 of 1

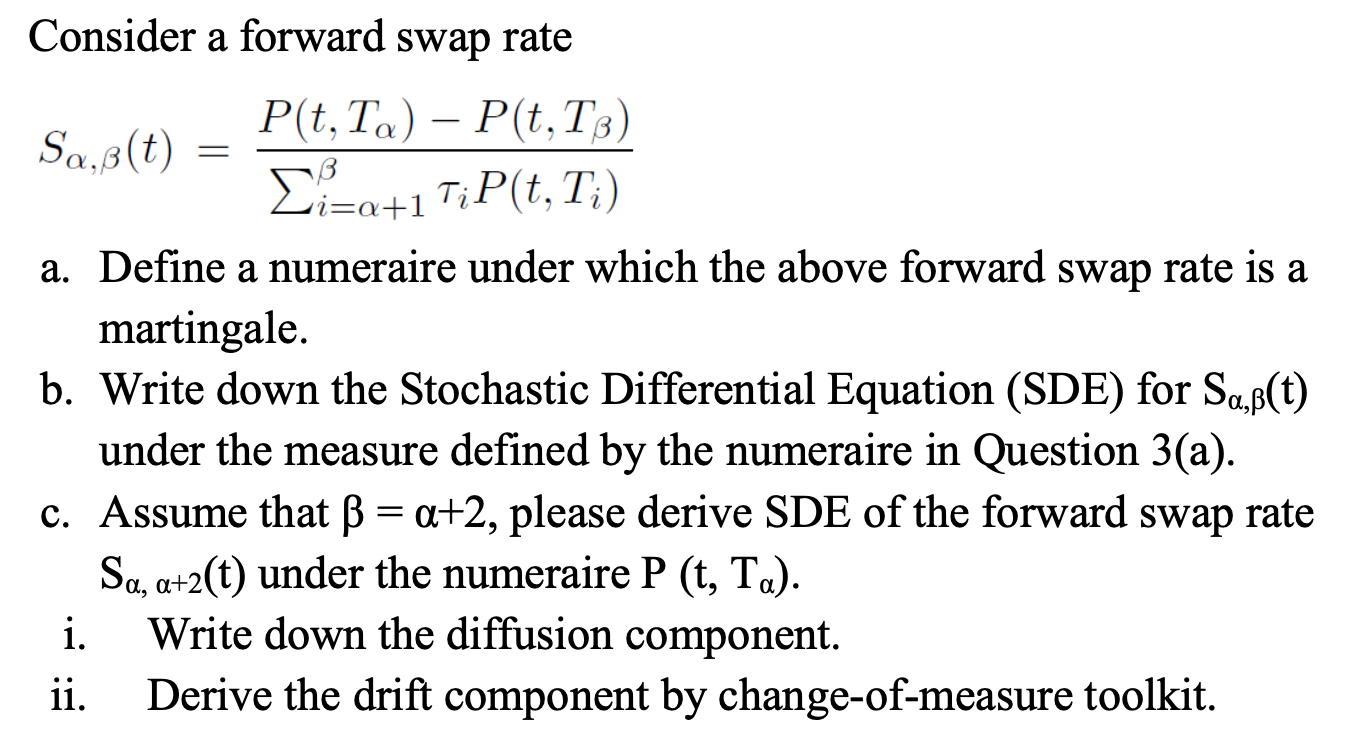

a . = Consider a forward swap rate P(t, T.) – P(t,T3) Sa,8(t) Σ41 τη Ρ(t, T:) a. Define a numeraire under which the abov

Posted: Wed May 11, 2022 7:03 pm

by answerhappygod

- 1 (133.44 KiB) Viewed 37 times

a . = Consider a forward swap rate P(t, T.) – P(t,T3) Sa,8(t) Σ41 τη Ρ(t, T:) a. Define a numeraire under which the above forward swap rate is a martingale. b. Write down the Stochastic Differential Equation (SDE) for Sa,f(t) under the measure defined by the numeraire in Question 3(a). c. Assume that ß = a+2, please derive SDE of the forward swap rate Sa, a+2(t) under the numeraire P (t, Ta). i. Write down the diffusion component. ii. Derive the drift component by change-of-measure toolkit. = +