Page 1 of 1

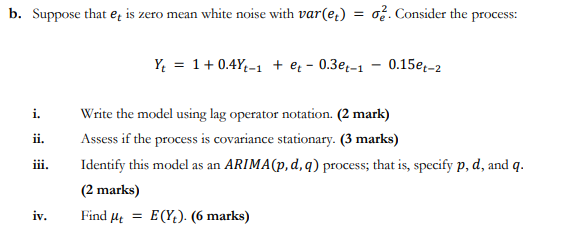

b. Suppose that eis zero mean white noise with var(e) = 02. Consider the process: Yo = 1 + 0.44,-1 + € - 0.3et-1 – 0.15e

Posted: Wed May 11, 2022 5:15 pm

by answerhappygod

- B Suppose That Eis Zero Mean White Noise With Var E 02 Consider The Process Yo 1 0 44 1 0 3et 1 0 15e 1 (35.16 KiB) Viewed 32 times

b. Suppose that eis zero mean white noise with var(e) = 02. Consider the process: Yo = 1 + 0.44,-1 + € - 0.3et-1 – 0.15et-2 i. ii. iii. Write the model using lag operator notation. (2 mark) Assess if the process is covariance stationary. (3 marks) Identify this model as an ARIMA(p, d,q) process; that is, specify p, d, and q. (2 marks) Find Me = E(Y). (6 marks) iv.