Page 1 of 1

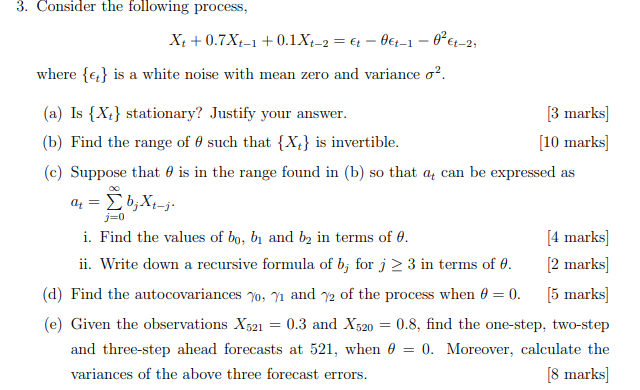

3. Consider the following process, X: +0.7X4–1 +0.1X1-2 = £t -0€-1 - 6 € -2, where {e} is a white noise with mean zero a

Posted: Wed May 11, 2022 9:30 am

by answerhappygod

- 3 Consider The Following Process X 0 7x4 1 0 1x1 2 T 0 1 6 2 Where E Is A White Noise With Mean Zero A 1 (71.82 KiB) Viewed 35 times

3. Consider the following process, X: +0.7X4–1 +0.1X1-2 = £t -0€-1 - 6 € -2, where {e} is a white noise with mean zero and variance op. j=0 (a) Is {Xt} stationary? Justify your answer. [3 marks] (b) Find the range of O such that {X;} is invertible. [10 marks) (C) Suppose that is in the range found in (b) so that ay can be expressed as α, = ΣΕ, Χ-5. i. Find the values of bo, b, and by in terms of 0. [4 marks] ii. Write down a recursive formula of b; for j> 3 in terms of e. [2 marks] (d) Find the autocovariances 70, 71 and 72 of the process when 0 = 0. [5 marks] (e) Given the observations X521 = 0.3 and X520 = 0.8, find the one-step, two-step and three-step ahead forecasts at 521, when 0 = 0. Moreover, calculate the variances of the above three forecast errors. [8 marks]