Page 1 of 1

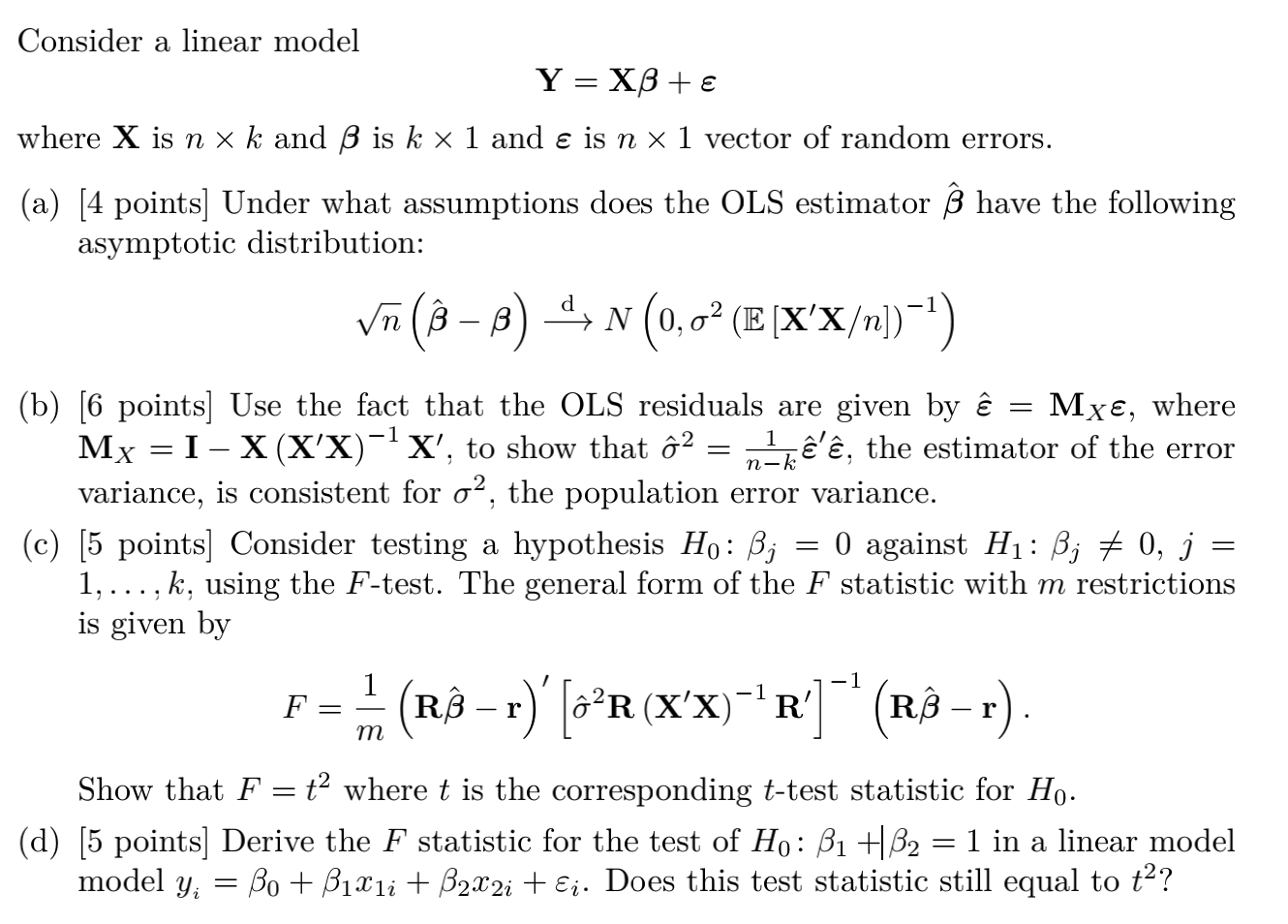

Consider a linear model Y = XB + € where X is n x k and ß is k x 1 and ε is n x 1 vector of random errors. (a) [4 points

Posted: Wed May 11, 2022 8:30 am

by answerhappygod

- 1 (178.21 KiB) Viewed 29 times

Consider a linear model Y = XB + € where X is n x k and ß is k x 1 and ε is n x 1 vector of random errors. (a) [4 points] Under what assumptions does the OLS estimator ß have the following asymptotic distribution: Vn (B – B) 44 n (0,0? (E [X'X/n])-1) В = -1 = = . - (b) [6 points] Use the fact that the OLS residuals are given by ê Mxe, where My = I – X(X'X)-? X', to show that ô2 = nhiê'ê, the estimator of the error variance, is consistent for o>, the population error variance. (c) [5 points] Consider testing a hypothesis Ho: B; O against Hı: B; + 0, j 1, ..., k, using the F-test. The general form of the F statistic with m restrictions is given by : = -1 -1 F = (RB – r)' [GPR (X'X)-'R)** (RB ) – r). 2R m Show that F t2 where t is the corresponding t-test statistic for Ho. (d) [5 points] Derive the F statistic for the test of Ho: B1 +182 1 in a linear model model y; = Bo + Bixli + B2X2i + εi. Does this test statistic still equal to t2? =