Page 1 of 1

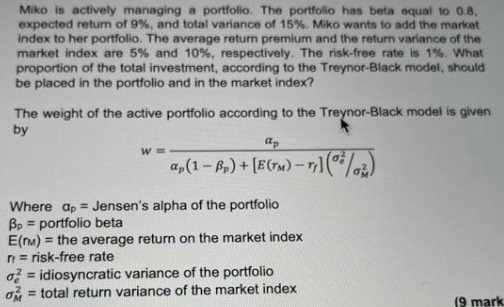

Miko is actively managing a portfolio. The portfolio has beta equal to 0.8, expected return of 9%, and total variance of

Posted: Wed May 11, 2022 6:04 am

by answerhappygod

- Miko Is Actively Managing A Portfolio The Portfolio Has Beta Equal To 0 8 Expected Return Of 9 And Total Variance Of 1 (181.88 KiB) Viewed 15 times

Miko is actively managing a portfolio. The portfolio has beta equal to 0.8, expected return of 9%, and total variance of 15%. Miko wants to add the market index to her portfolio. The average return premium and the return variance of the market index are 5% and 10%, respectively. The risk-free rate is 1%. What proportion of the total investment, according to the Treynor-Black model, should be placed in the portfolio and in the market index? The weight of the active portfolio according to the Treynor-Black model is given by ap W= 3,1 – 6,) + (EP) - (*) - Where Qp = Jensen's alpha of the portfolio Bp = portfolio beta E(rm) = the average return on the market index r = risk-free rate 0} = idiosyncratic variance of the portfolio on = total return variance of the market index 19 mark