Page 1 of 1

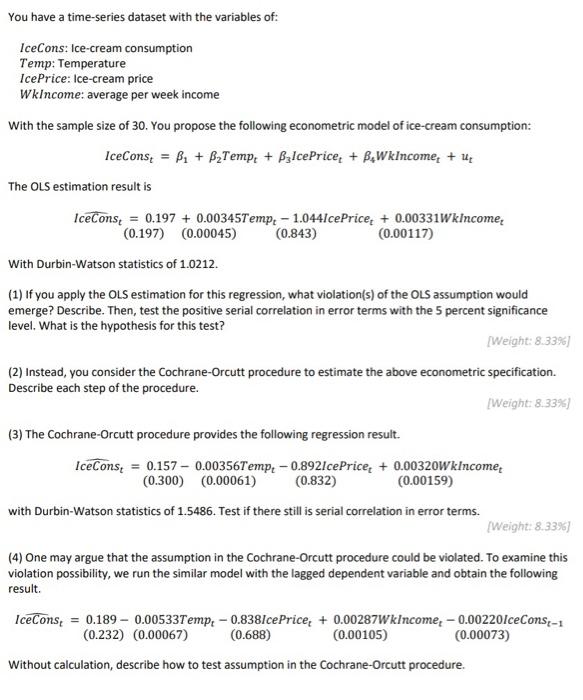

You have a time-series dataset with the variables of: IceCons: Ice-cream consumption Temp: Temperature IcePrice: Ice-cre

Posted: Wed May 11, 2022 5:57 am

by answerhappygod

- You Have A Time Series Dataset With The Variables Of Icecons Ice Cream Consumption Temp Temperature Iceprice Ice Cre 1 (62 KiB) Viewed 46 times

You have a time-series dataset with the variables of: IceCons: Ice-cream consumption Temp: Temperature IcePrice: Ice-cream price WkIncome: average per week income With the sample size of 30. You propose the following econometric model of ice-cream consumption: IceCons= B1 + B2Temp: + BzIcePrice+ B.WkIncome + 4 The OLS estimation result is IceCons = 0.197 + 0.00345Temp. - 1.044IcePrice: + 0.00331Wkincome, (0.197) (0.00045) (0.843) (0.00117) With Durbin-Watson statistics of 1.0212. (1) If you apply the OLS estimation for this regression, what violation(s) of the OLS assumption would emerge? Describe. Then, test the positive serial correlation in error terms with the 5 percent significance level. What is the hypothesis for this test? Weight: 8.33%) (2) Instead, you consider the Cochrane-Orcutt procedure to estimate the above econometric specification. Describe each step of the procedure. Weight: 8.33%) (3) The Cochrane-Orcutt procedure provides the following regression result IceConsę = 0.157 - 0.00356Temp. - 0.892IcePrice + 0.00320WkIncome (0.300) (0.00061) (0.832) (0.00159) with Durbin-Watson statistics of 1.5486. Test if there still is serial correlation in error terms. Weight: 8.33%) (4) One may argue that the assumption in the Cochrane-Orcutt procedure could be violated. To examine this violation possibility, we run the similar model with the lagged dependent variable and obtain the following result. IceCons = 0.189 -0.00533Temp. - 0.838IcePrice+ 0.00287WkIncome, -0.00220IceCons-1 (0.232) (0.00067) (0.688) (0.00105) (0.00073) Without calculation, describe how to test assumption in the Cochrane-Orcutt procedure.