Page 1 of 1

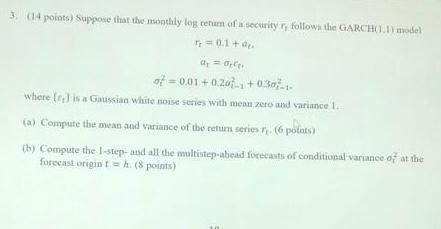

3(14 points) Suppose that the monthly log return of a security ry follows the GARCHI model 0.1 + a=0 of = 0.01 +0.20 +03

Posted: Tue May 10, 2022 6:31 am

by answerhappygod

- 3 14 Points Suppose That The Monthly Log Return Of A Security Ry Follows The Garchi Model 0 1 A 0 Of 0 01 0 20 03 1 (9.66 KiB) Viewed 29 times

3(14 points) Suppose that the monthly log return of a security ry follows the GARCHI model 0.1 + a=0 of = 0.01 +0.20 +030... where is a Gaussian white noise series with mean zero and variance (a) Compute the mean and variance of the retum series (6 potets) (b) Compute the I-step- and all the multistep-ahead forecasts of conditional variance of at the forecast origin = h. (8 points)