Page 1 of 1

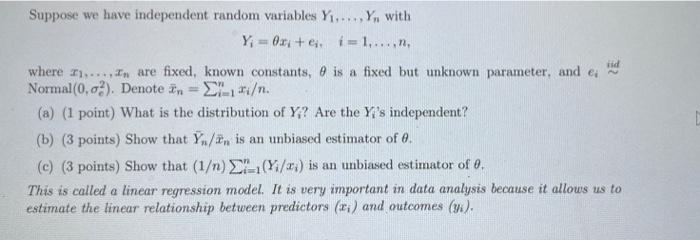

Suppose we have independent random variables Y1...,Y, with Y; = 0,+ i1,...,n. where )..... In are fixed, known constants

Posted: Sun Oct 03, 2021 3:33 pm

by answerhappygod

- Suppose We Have Independent Random Variables Y1 Y With Y 0 I1 N Where In Are Fixed Known Constants 1 (26.12 KiB) Viewed 147 times

Suppose we have independent random variables Y1...,Y, with Y; = 0,+ i1,...,n. where )..... In are fixed, known constants, 9 is a fixed but unknown parameter, and e; Normal(0,0%). Denote in"/n. (a) (1 point) What is the distribution of Y,? Are the Yi's independent? (b) (3 points) Show that Y/t, is an unbiased estimator of e. © (3 points) Show that (1/n), (Y/x) is an unbiased estimator of 0. This is called a linear regression model. It is very important in data analysis because it allows us to estimate the linear relationship between predictors (ri) and outcomes (w).