Page 1 of 1

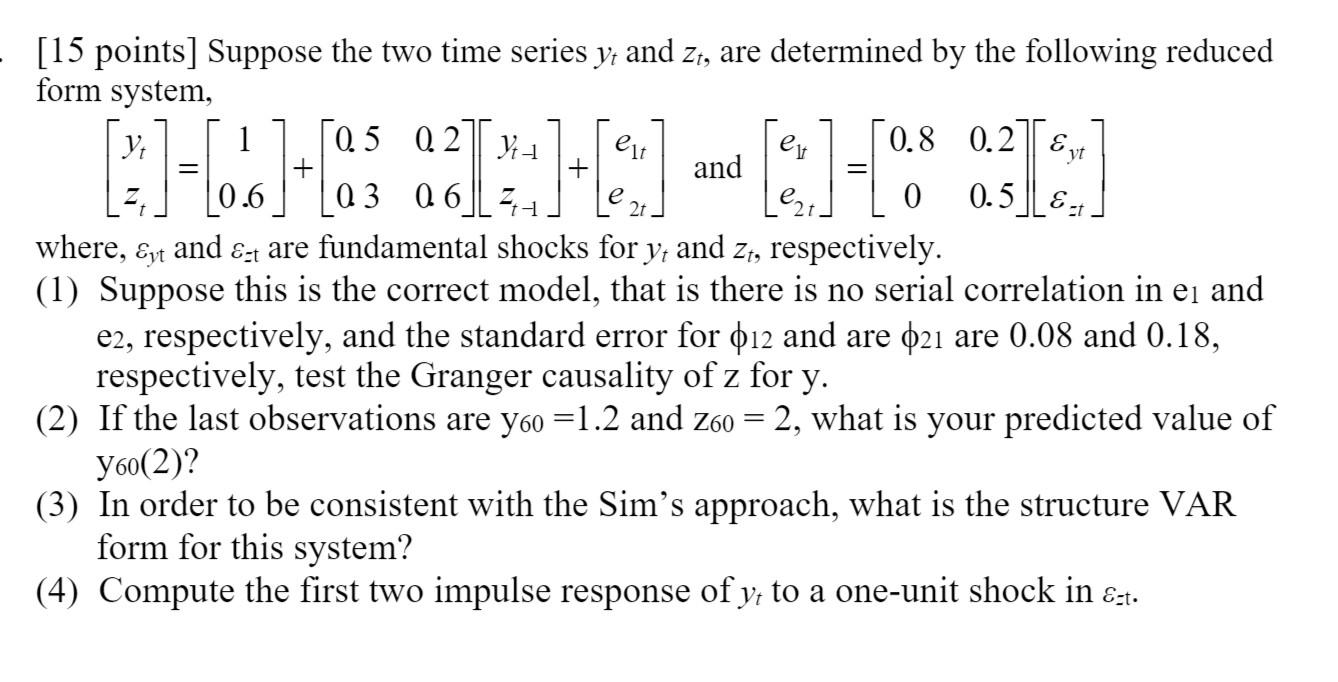

0.2 || Ytt ( 31-07-03 13:1-93-(2H-alle 3 + e 0.5 || 8 [15 points] Suppose the two time series y; and zt, are determined

Posted: Mon May 09, 2022 12:43 pm

by answerhappygod

- 0 2 Ytt 31 07 03 13 1 93 2h Alle 3 E 0 5 8 15 Points Suppose The Two Time Series Y And Zt Are Determined 1 (115.68 KiB) Viewed 21 times

0.2 || Ytt ( 31-07-03 13:1-93-(2H-alle 3 + e 0.5 || 8 [15 points] Suppose the two time series y; and zt, are determined by the following reduced form system, 0.5 ent 0.8 0.2 || & yt and 0.6 (6L241 0 where, Eyt and ezt are fundamental shocks for y; and zt, respectively. Yt (1) Suppose this is the correct model, that is there is no serial correlation in ei and e2, respectively, and the standard error for 012 and are 021 are 0.08 and 0.18, respectively, test the Granger causality of z for y. z (2) If the last observations are y60 =1.2 and 260 2, what is your predicted value of Y60(2)? (3) In order to be consistent with the Sim's approach, what is the structure VAR form for this system? (4) Compute the first two impulse response of y; to a one-unit shock in Est.