Page 1 of 1

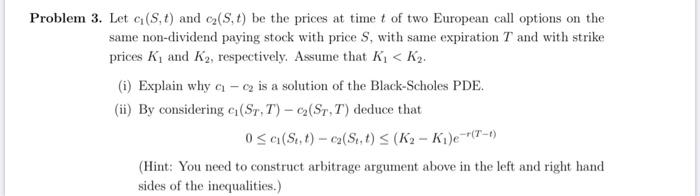

Problem 3. Let G(S,t) and cz(S. t) be the prices at time t of two European call options on the same non-dividend paying

Posted: Mon May 09, 2022 12:07 pm

by answerhappygod

- Problem 3 Let G S T And Cz S T Be The Prices At Time T Of Two European Call Options On The Same Non Dividend Paying 1 (19.41 KiB) Viewed 23 times

Problem 3. Let G(S,t) and cz(S. t) be the prices at time t of two European call options on the same non-dividend paying stock with price S, with same expiration T and with strike prices K and K2, respectively. Assume that Ki <K2. (1) Explain why & -o is a solution of the Black-Scholes PDE. (ii) By considering (Sr, T) - (Sr, T) deduce that OSA(S..t) - ca(S. t) S (K2 - Ki)e-(7-6) (Hint: You need to construct arbitrage argument above in the left and right hand sides of the inequalities.)