Page 1 of 1

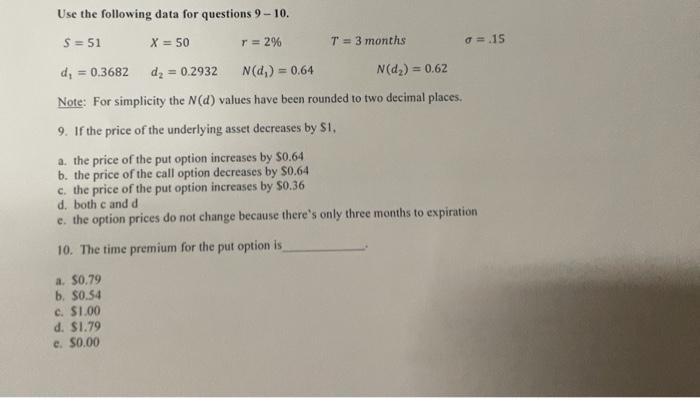

Use the following data for questions 9-10. S = 51 X = 50 r = 2% T = 3 months o=15 di = 0.3682 dx = 0.2932 N(d) = 0.64 N(

Posted: Sun May 08, 2022 10:43 am

by answerhappygod

- Use The Following Data For Questions 9 10 S 51 X 50 R 2 T 3 Months O 15 Di 0 3682 Dx 0 2932 N D 0 64 N 1 (23.55 KiB) Viewed 36 times

Use the following data for questions 9-10. S = 51 X = 50 r = 2% T = 3 months o=15 di = 0.3682 dx = 0.2932 N(d) = 0.64 N(d) = 0.62 Note: For simplicity the N(d) values have been rounded to two decimal places. 9. If the price of the underlying asset decreases by S1. a. the price of the put option increases by $0.64 b. the price of the call option decreases by $0.64 c. the price of the put option increases by S0.36 d. both c and d c. the option prices do not change because there's only three months to expiration 10. The time premium for the put option is a. $0.79 b. $0,54 c. $1.00 d. $1.79 e. $0.00