Page 1 of 1

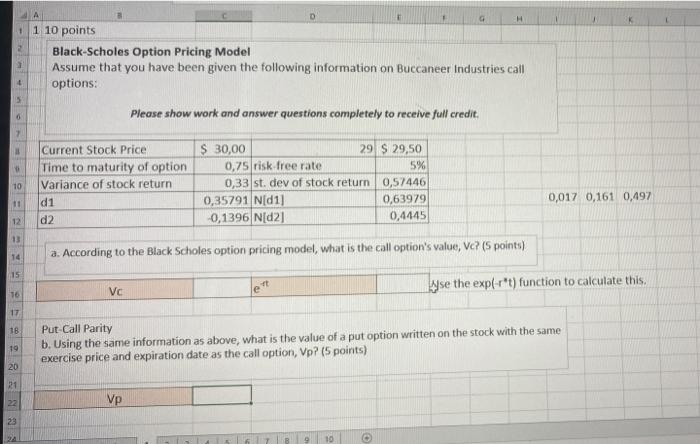

A G H + 1 10 points Black-Scholes Option Pricing Model Assume that you have been given the following information on Bucc

Posted: Sun May 08, 2022 10:42 am

by answerhappygod

- A G H 1 10 Points Black Scholes Option Pricing Model Assume That You Have Been Given The Following Information On Bucc 1 (48.3 KiB) Viewed 67 times

A G H + 1 10 points Black-Scholes Option Pricing Model Assume that you have been given the following information on Buccaneer Industries call options: 5 0 Please show work and answer questions completely to receive full credit. 7 10 Current Stock Price Time to maturity of option Variance of stock return d1 d2 $ 30,00 29 $ 29,50 0,75 risk free rate 5% 0,33 st. dev of stock return 0,57446 0,35791 N[d1] 0,63979 -0,1396 N[02] 0,4445 0,017 0,161 0,497 11 12 13 14 a. According to the Black Scholes option pricing model, what is the call option's value, Vc? (5 points) 15 16 Vc yse the expl-r*t) function to calculate this. em 17 18 Put-Call Parity b. Using the same information as above, what is the value of a put option written on the stock with the same exercise price and expiration date as the call option, Vp? (5 points) 19 20 21 22 Vp 23