Page 1 of 1

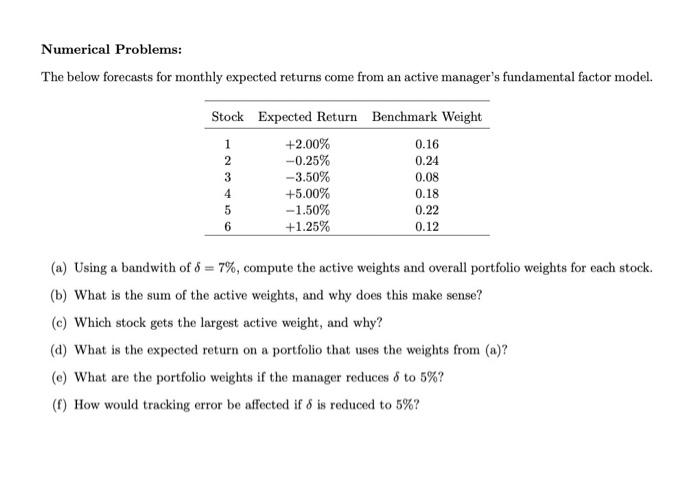

Numerical Problems: The below forecasts for monthly expected returns come from an active manager's fundamental factor mo

Posted: Sun May 08, 2022 10:07 am

by answerhappygod

- Numerical Problems The Below Forecasts For Monthly Expected Returns Come From An Active Manager S Fundamental Factor Mo 1 (33.39 KiB) Viewed 28 times

Numerical Problems: The below forecasts for monthly expected returns come from an active manager's fundamental factor model. Stock Expected Return Benchmark Weight 1 +2.00% 0.16 2 -0.25% 0.24 -3.50% 0.08 +5.00% 0.18 5 -1.50% 0.22 6 +1.25% 0.12 3 (a) Using a bandwith of 8 = 7%, compute the active weights and overall portfolio weights for each stock. (b) What is the sum of the active weights, and why does this make sense? (c) Which stock gets the largest active weight, and why? (d) What is the expected return on a portfolio that uses the weights from (a)? (e) What are the portfolio weights if the manager reduces 8 to 5%? (1) How would tracking error be affected if & is reduced to 5%?