Page 1 of 1

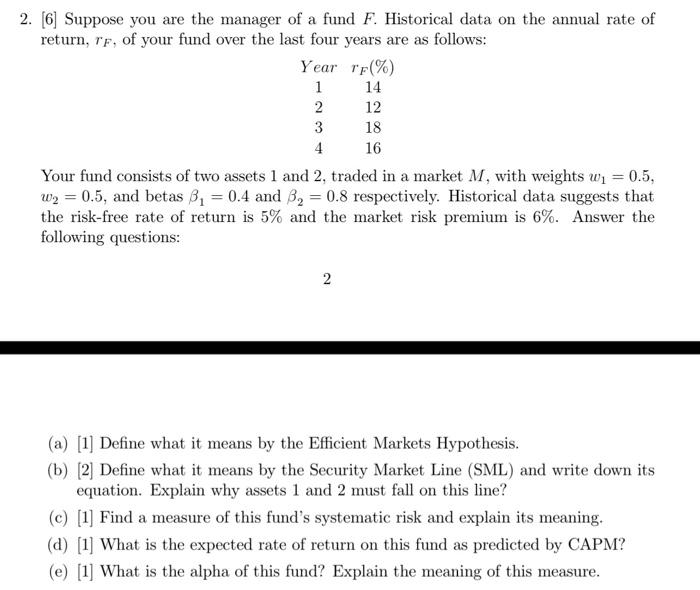

2. [6] Suppose you are the manager of a fund F. Historical data on the annual rate of return, rf, of your fund over the

Posted: Sun May 08, 2022 9:59 am

by answerhappygod

- 2 6 Suppose You Are The Manager Of A Fund F Historical Data On The Annual Rate Of Return Rf Of Your Fund Over The 1 (52.45 KiB) Viewed 29 times

2. [6] Suppose you are the manager of a fund F. Historical data on the annual rate of return, rf, of your fund over the last four years are as follows: Year F(%) 1 14 2 12 3 4 16 Your fund consists of two assets 1 and 2, traded in a market M, with weights w1 = 0.5, W2 = 0.5, and betas B= 0.4 and B2 = 0.8 respectively. Historical data suggests that the risk-free rate of return is 5% and the market risk premium is 6%. Answer the following questions: 18 2 (a) [1] Define what it means by the Efficient Markets Hypothesis. (b) [2] Define what it means by the Security Market Line (SML) and write down its equation. Explain why assets 1 and 2 must fall on this line? (C) [1] Find a measure of this fund's systematic risk and explain its meaning. (d) [1] What is the expected rate of return on this fund as predicted by CAPM? (e) [1] What is the alpha of this fund? Explain the meaning of this measure.