Page 1 of 1

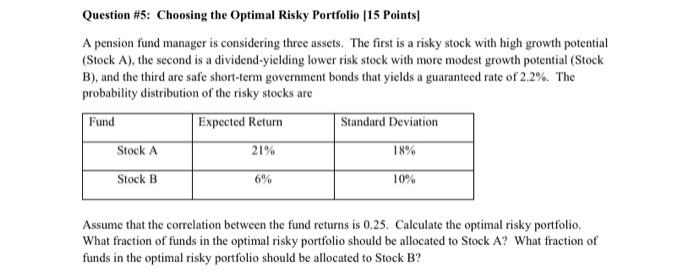

Question #5: Choosing the optimal Risky Portfolio [15 Points A pension fund manager is considering three assets. The fir

Posted: Sun May 08, 2022 8:49 am

by answerhappygod

- Question 5 Choosing The Optimal Risky Portfolio 15 Points A Pension Fund Manager Is Considering Three Assets The Fir 1 (29.18 KiB) Viewed 34 times

Question #5: Choosing the optimal Risky Portfolio [15 Points A pension fund manager is considering three assets. The first is a risky stock with high growth potential (Stock A), the second is a dividend-yielding lower risk stock with more modest growth potential (Stock B), and the third are safe short-term government bonds that yields a guaranteed rate of 2.2%. The probability distribution of the risky stocks are Fund Expected Return Standard Deviation Stock A 21% 18% Stock B 10% Assume that the correlation between the fund returns is 0.25. Calculate the optimal risky portfolio. What fraction of funds in the optimal risky portfolio should be allocated to Stock A? What fraction of funds in the optimal risky portfolio should be allocated to Stock B?