Page 1 of 1

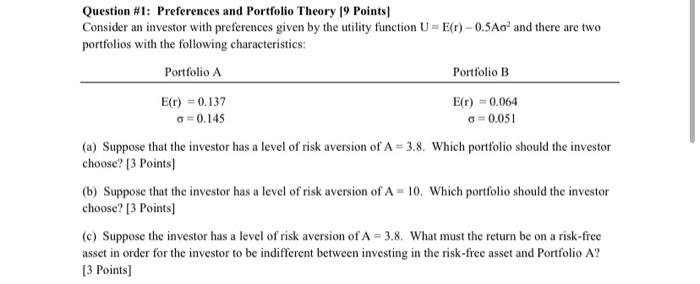

Question #1: Preferences and Portfolio Theory 19 Points Consider an investor with preferences given by the utility funct

Posted: Sun May 08, 2022 8:48 am

by answerhappygod

- Question 1 Preferences And Portfolio Theory 19 Points Consider An Investor With Preferences Given By The Utility Funct 1 (25.28 KiB) Viewed 24 times

Question #1: Preferences and Portfolio Theory 19 Points Consider an investor with preferences given by the utility function U = E(r) -0.5Ao' and there are two portfolios with the following characteristics: Portfolio A Portfolio B E(r) = 0.137 E() -0,064 o=0.145 0 =0.051 (a) Suppose that the investor has a level of risk aversion of A = 3.8. Which portfolio should the investor choose? (3 Points (b) Suppose that the investor has a level of risk aversion of A-10. Which portfolio should the investor choose? [3 Points) (C) Suppose the investor has a level of risk aversion of A = 3.8. What must the return be on a risk-free asset in order for the investor to be indifferent between investing in the risk-free asset and Portfolio A? [3 Points)