Page 1 of 1

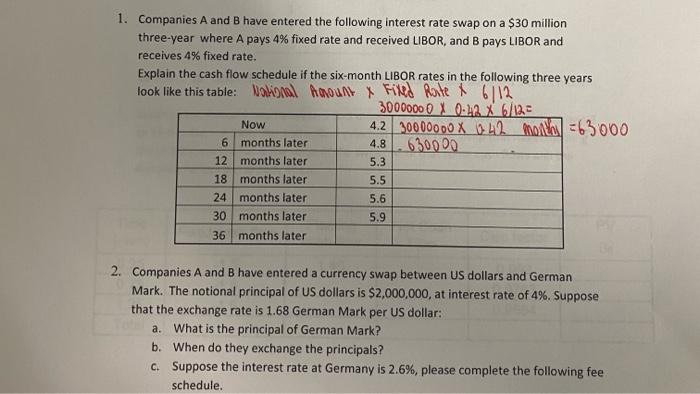

1. Companies A and B have entered the following interest rate swap on a $30 million three-year where A pays 4% fixed rat

Posted: Fri May 06, 2022 7:13 am

by answerhappygod

- 1 Companies A And B Have Entered The Following Interest Rate Swap On A 30 Million Three Year Where A Pays 4 Fixed Rat 1 (41.43 KiB) Viewed 26 times

1. Companies A and B have entered the following interest rate swap on a $30 million three-year where A pays 4% fixed rate and received LIBOR, and B pays LIBOR and receives 4% fixed rate. Explain the cash flow schedule if the six-month LIBOR rates in the following three years look like this table: National Account x Fixed Rate X 6/12 300000000-42 X 6/12 = Now 4.2 30000000 X 42 month=63000 4.8 630000 6 months later 12 months later. 5.3 18 months later 5.5 24 months later 5.6 30 months later 5.9 36 months later 2. Companies A and B have entered a currency swap between US dollars and German Mark. The notional principal of US dollars is $2,000,000, at interest rate of 4%. Suppose that the exchange rate is 1.68 German Mark per US dollar: a. What is the principal of German Mark? b. When do they exchange the principals? c. Suppose the interest rate at Germany is 2.6%, please complete the following fee schedule.