Page 1 of 1

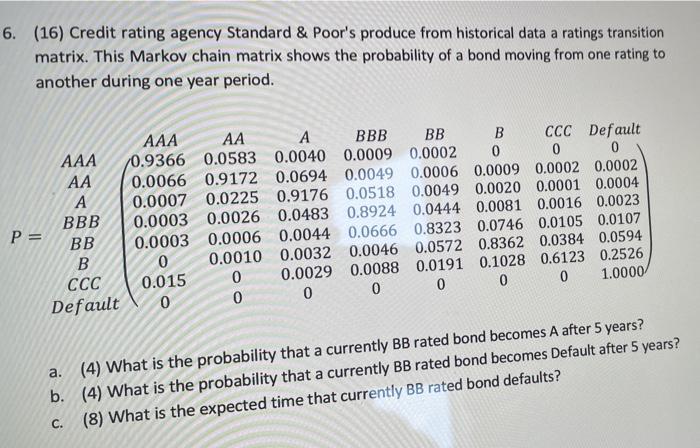

6. (16) Credit rating agency Standard & Poor's produce from historical data a ratings transition matrix. This Markov cha

Posted: Thu May 05, 2022 9:13 pm

by answerhappygod

- 6 16 Credit Rating Agency Standard Poor S Produce From Historical Data A Ratings Transition Matrix This Markov Cha 1 (65.27 KiB) Viewed 33 times

6. (16) Credit rating agency Standard & Poor's produce from historical data a ratings transition matrix. This Markov chain matrix shows the probability of a bond moving from one rating to another during one year period. AAA AA A BBB BB B CCC AAA Default 0 0 0 AA A 0.9366 0.0583 0.0040 0.0009 0.0002 0.0066 0.9172 0.0694 0.0049 0.0006 0.0009 0.0002 0.0002 0.0049 0.0020 0.0001 0.0004 0.0444 0.0081 0.0016 0.0023 0.8323 0.0746 0.0105 0.0107 0.0572 0.8362 0.0384 0.0594 0.0191 0.1028 0.6123 0.2526 0.0007 0.0225 0.0003 0.0026 BBB BB 0.0003 0.9176 0.0518 0.0483 0.8924 0.0006 0.0044 0.0666 0.0032 0.0046 0.0029 0.0088 B 0 0.0010 0 CCC 0.015 0 1.0000 0 0 0 Default 0 0 0 a. (4) What is the probability that a currently BB rated bond becomes A after 5 years? b. (4) What is the probability that a currently BB rated bond becomes Default after 5 years? c. (8) What is the expected time that currently BB rated bond defaults? P =