Page 1 of 1

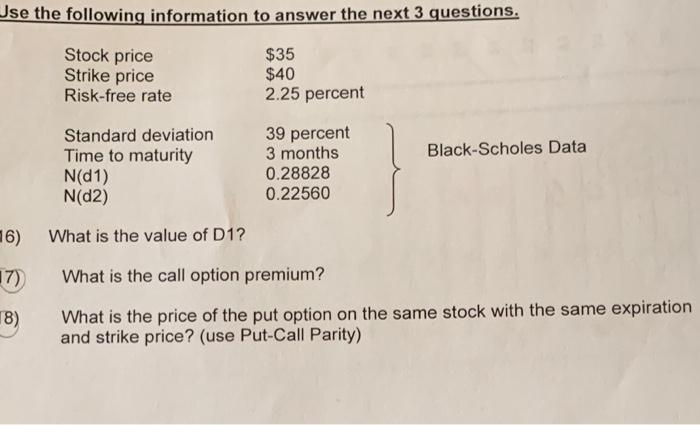

Use the following information to answer the next 3 questions. Stock price Strike price Risk-free rate $35 $40 2.25 perce

Posted: Thu May 05, 2022 8:21 am

by answerhappygod

- Use The Following Information To Answer The Next 3 Questions Stock Price Strike Price Risk Free Rate 35 40 2 25 Perce 1 (31.61 KiB) Viewed 35 times

Use the following information to answer the next 3 questions. Stock price Strike price Risk-free rate $35 $40 2.25 percent Standard deviation 39 percent 3 months Time to maturity Black-Scholes Data N(D1) 0.28828 N(D2) 0.22560 16) What is the value of D1? (7) What is the call option premium? 8) What is the price of the put option on the same stock with the same expiration and strike price? (use Put-Call Parity)