Page 1 of 1

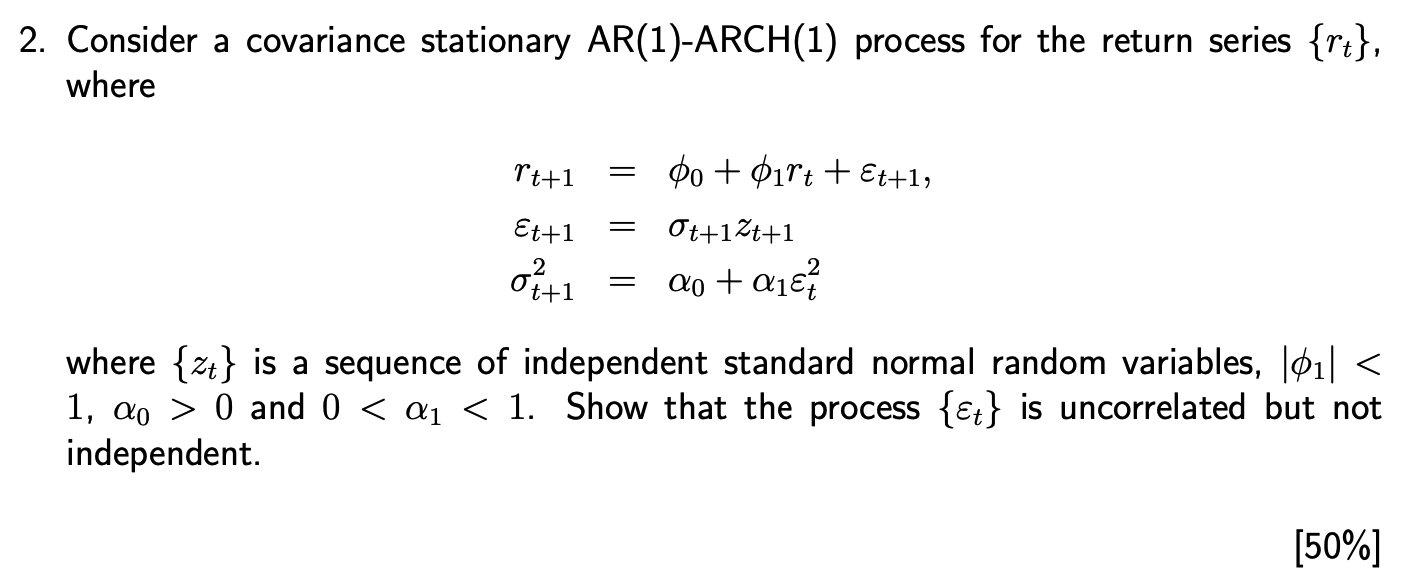

2. Consider a covariance stationary AR(1)-ARCH(1) process for the return series {rt}, where rt+1 do + 1rt + Et+1, Et+1 =

Posted: Wed May 04, 2022 1:24 pm

by answerhappygod

- 2 Consider A Covariance Stationary Ar 1 Arch 1 Process For The Return Series Rt Where Rt 1 Do 1rt Et 1 Et 1 1 (54.04 KiB) Viewed 43 times

2. Consider a covariance stationary AR(1)-ARCH(1) process for the return series {rt}, where rt+1 do + 1rt + Et+1, Et+1 = Ot+12t+1 2 of+1 = α0 + α1€ ²² where {2} is a sequence of independent standard normal random variables, |¢1| < 1, ª > 0 and 0 < α₁ < 1. Show that the process {} is uncorrelated but not independent. [50%]