Page 1 of 1

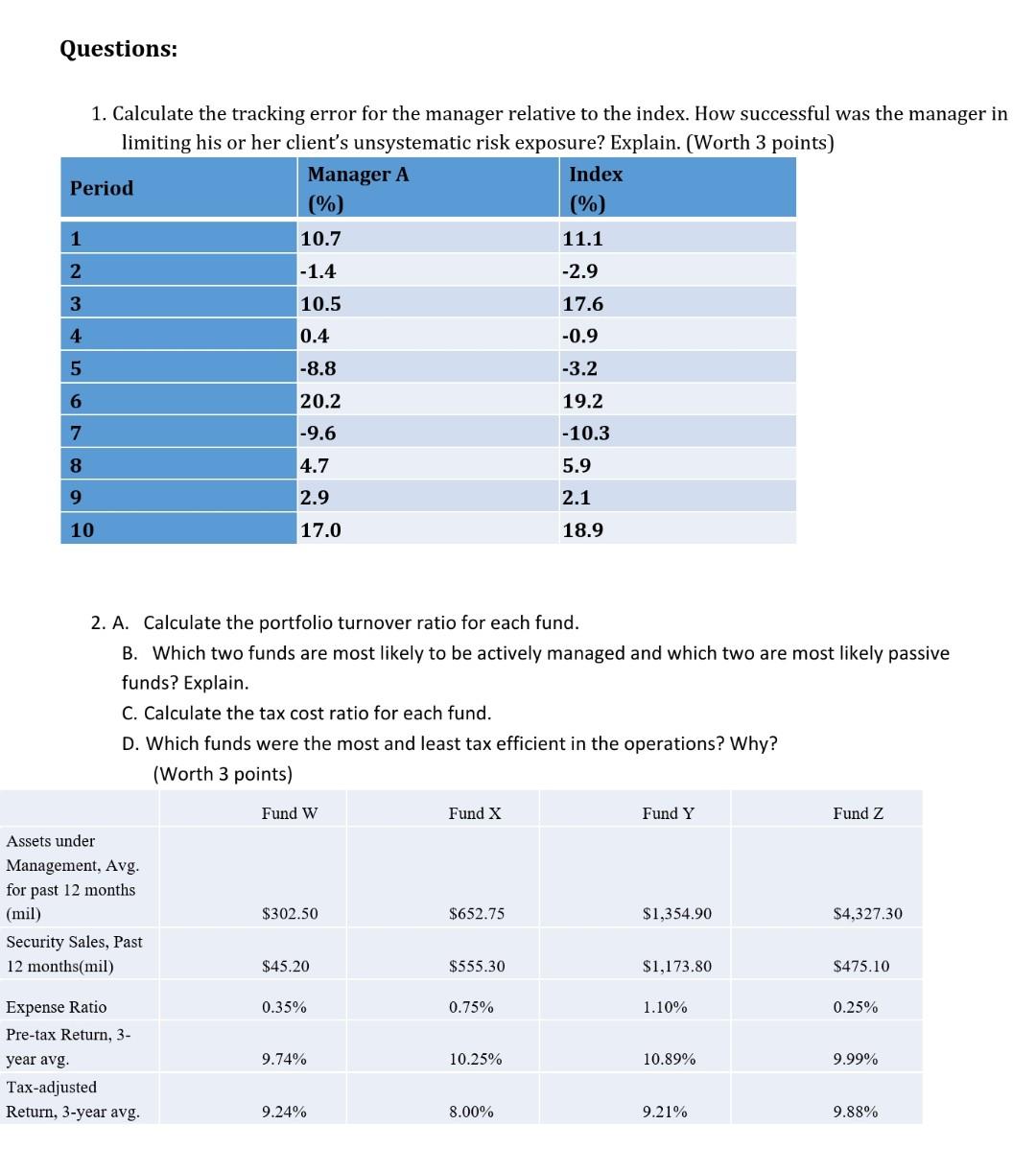

Questions: 1. Calculate the tracking error for the manager relative to the index. How successful was the manager in limi

Posted: Mon May 02, 2022 9:02 am

by answerhappygod

- Questions 1 Calculate The Tracking Error For The Manager Relative To The Index How Successful Was The Manager In Limi 1 (110.26 KiB) Viewed 33 times

Questions: 1. Calculate the tracking error for the manager relative to the index. How successful was the manager in limiting his or her client's unsystematic risk exposure? Explain. (Worth 3 points) Manager A Index Period (%) (%) 1 10.7 11.1 2 -1.4 -2.9 3 10.5 17.6 4 0.4 -0.9 5 -8.8 -3.2 6 20.2 19.2 -10.3 7 -9.6 8 4.7 5.9 9 2.9 2.1 10 17.0 18.9 2. A. Calculate the portfolio turnover ratio for each fund. B. Which two funds are most likely to be actively managed and which two are most likely passive funds? Explain. C. Calculate the tax cost ratio for each fund. D. Which funds were the most and least tax efficient in the operations? Why? (Worth 3 points) Fund w Fund X Fund Y Fund Z Assets under Management, Avg. for past 12 months (mil) Security Sales, Past 12 months(mil) $302.50 $652.75 $1,354.90 $4,327.30 $45.20 $555.30 $1,173.80 $475.10 0.35% 0.75% 1.10% 0.25% Expense Ratio Pre-tax Return, 3- year avg. Tax-adjusted Return, 3-year avg. 9.74% 10.25% 10.89% 9.99% 9.24% 8.00% 9.21% 9.88%